Buyers Beware: Loan Shark Harassment

Imagine purchasing your dream home for a good price in a beloved neighbourhood, only to have it transform into a living nightmare overnight, when loan shark runners started showing up. Suddenly, you find yourself at the receiving end of relentless harassment, despite having no prior dealings with any unlicensed money lenders.

Such an unfortunate turn of events happened to one homeowner. According to an online forum post back in May 2009, a home owner claimed that his resale unit was splashed with red paint, no thanks to the previous owner of the unit who had allegedly borrowed money from loan sharks.

Although the chances of such predicament occurring are generally low, homebuyers may still want to conduct thorough due diligence before finalising a property purchase. While most buyers are vigilant about issues such as leaky pipes, poor plumbing, spalling concrete, a mould problem, popping floor tiles, or even noisy neighbours, they may not necessarily check for loan shark harassment (if any). Most issues are visible to the naked eye, but loan shark harassment may be covered up by a fresh coat of paint, so that new owners need not spend money to repaint the premise; an attractive price, because the sellers are migrating soon; among other smokescreens.

Loan shark harassment can involve a range of aggressive tactics, including splashing paint on the properties, vandalising walls with graffiti, and posting threatening messages on doors, in the stairwell or common corridor. Some loan sharks also resort to threatening family members, stalking and embarrassing the debtors. These are common methods used by unlicensed money lenders to intimidate and pressure debtors.

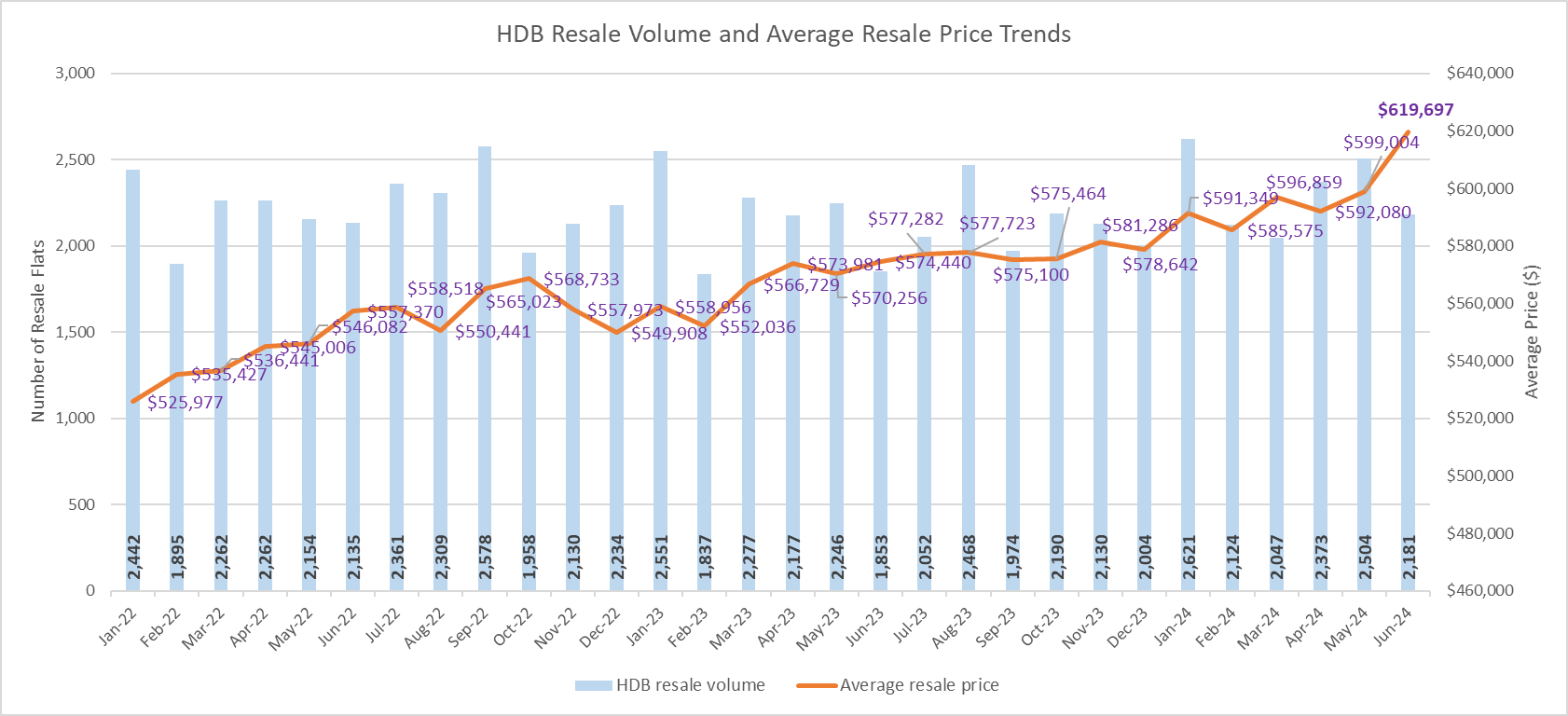

To be sure, the incidences of illegal money lending activities as a proportion of homes in Singapore is extremely low. In an AsiaOne article dated 21 June 2024, it was reported that there were more than 2,800 harassment cases in 2022, down from over 4,600 cases in 2018. Not all cases involve properties, and comparing this to the number of residential properties in Singapore today which is more than 1.4 million units, the number is negligible.

It was also reported that some loan sharks have shifted to digital tactics to avoid getting caught by the authorities. These include spam-calling the workplace of the debtor, posting on social media platforms using anonymous accounts to scare or shame debtors, or placing and sending large orders via online food delivery platforms that require cash-on-delivery to the debtor's home.

The next question is: Are sellers and their appointed real estate salesperson ("RES") legally obligated to disclose any outstanding loan shark debts to prospective buyers?

Currently, there are no statutory requirements or codes of practice mandating the voluntary disclosure of loan shark harassment by sellers. However, according to para 3.8.3(d) of the Professional Services Manual issued by the Council for Estate Agencies, the seller's appointed RES is obliged to find out from his client and convey material information on the property - including loan shark harassment - when asked by the buyer or the buyer's RES.

Prospective buyers can look out for any potential signs of loan shark harassment during the property viewing. Should they be concerned about any such activities, the buyer or the buyer's RES can seek clarification from the seller or the seller's RES too as mentioned above.

Here are some potential red flags to look out for during property viewings:

CCTV cameras installed outside their homes

As of May 2023, the Housing and Development Board (HDB) no longer requires approval for installing corridor-facing CCTV cameras inside flats, provided they do not infringe on neighbours' privacy. However, cameras installed outside the HDB flat still require HDB's approval. While the seller might claim that the camera has been installed for seemingly innocent reasons, such as making sure the children get home from school, it could also be used to deter loan shark runners from vandalising property and carrying out harassment acts.

Fresh coat of paint on exterior walls

A fresh coat of paint on exterior walls or along the common corridor is a major red flag. Sellers typically repaint only the interior walls to prep for viewing. If the exterior walls look to have been recently repainted, it may be an attempt to cover up loan shark graffiti. That said, the seller could say the paint was done due to mould issues or a fresh-start-bonus-makeover to welcome new unsuspecting owners!

New locks and doors installed

Do the main door and gate look like that have just been replaced, or perhaps there is a new lock or multiple locks installed? These new doors and locks could be installed arising from vandalism or harassment by loan sharks, or to prevent forced entry by illegal debt collectors. But then again, the seller may claim the old locks were spoiled. Come to think of it, would a buyer notice the locks when the focus is on the house? In any case, the locks would normally be changed by the new owner for security reasons; hence not much notice will be placed on them.

Burn or scorch marks

Look for burn or scorch marks on corridors, walls, or the main door. Setting fire to property was a common loan shark harassment tactic used in the past to threaten debtors. Be sure to query the sellers or their appointed RES about any scorch marks outside the unit. But here's the thing, why would sellers leave burnt marks around for buyers to spot and quiz them?

Ask thy neighbour

Though it may seem intrusive, asking neighbors about any unusual activity can be informative, especially if you've noticed multiple red flags (see above). Neighbors may be willing to share what they know. Approach them politely when inquiring. But that said, what if the unit you desire is not affected by loan-shark activities, but the nice helpful neighbour is customer of loan sharks? Loan sharks are also known to harass neighbours to embarrass the loan defaulters.

Remember, the seller's RES is not legally required to disclose loan shark harassment at the property unless specifically asked by the buyer or buyer's salesperson. Therefore, it is crucial for buyers and their appointed RES to be vigilant and watch for signs of loan shark activity to avoid unwanted harassment from unlicensed money lenders.

When in doubt, always ask, but assuming you did ask, and the seller lied about it, what happens then? Also, what if the property you have purchased is not targeted by loan sharks but your neighbour's is? Or perhaps your neighbour becomes a loan shark contract defaulter after you have moved in, or the loan defaulter moved in next door a day after you? What if the loan shark harassment was scheduled to be carried out on the day you moved in because the customer defaulted in repayment a day before?

Check as you may and ask what you can, but it can be down to (bad) luck at times when it comes to such matters. But all hope is not lost.

If you find yourself the victim of loan shark harassment, there are steps you can take to address the situation effectively. Filing a police report is a straightforward process and can be done conveniently online. Showing the police report to the loan sharks or putting the report up on your door can act as a deterrent, and help prevent further harassment. You can file an e-police report at this link or call 999 in case of an emergency. For loan shark harassment specifically, you can also report it by calling the X-Ah Long hotline at 1800-924-5664.

The authorities continue to take tough enforcement action against those involved in such activities. Under the Moneylenders Act 2008, loan shark harassment is a serious offense, punishable by a fine of at least $5,000 and up to $50,000 AND imprisonment of up to five years AND up to six strokes of the cane. The number of strokes also increases if there are damage to property and/or cause hurt to another person (bodily harm, disease or infirmity).

It is assuring to know that Singapore's Police Force have zero tolerance for loan shark harassment activities. That said, most, if not all homebuyers would probably want to steer clear of such problems right from the start.

Oh no!

Enjoy our Content?

If it is of any consolation, know that you are not alone in this real estate journey. Let us show you the way to make this journey an interesting and enjoyable one!

Suggested Reads

Upcoming Events

View more

You may like

Holland Plain: The New Face of Prestige

May 13, 2026

Tokyo vs Singapore: Where Does Your Money Work Harder?

May 12, 2026

The 2026 Launch Rush Part 3: The Next Wave to Consider

May 08, 2026

New Price Record Set Despite Softer HDB Resale Market in April

May 06, 2026

Orchard's Next Big Thing: Paterson

May 05, 2026

Resale Landed Market Watch In March 2026

April 29, 2026