PropNex Picks

June 20, 2024

Think You're Ready to #BTOgether? Read This First!

Sheena Sugiarto

Research Writer

The dream of owning a home is one that many people share. Thankfully, the Housing Development Board (HDB) offers ways to make that a reality for Singapore citizens and permanent residents. The most prominent one? The Build-To-Order (BTO) scheme.

BTO is an affordable and quality housing option designed to help first-time home buyers and young families. Under this scheme, new residential flats are built by HDB and sold directly to eligible buyers. However, the process of getting a BTO flat can be complicated and daunting, especially if you're new to Singapore's property industry. This guide will tell you all you need to know about BTO and help you get through the process step by step.

Why BTO?

BTO offers compelling benefits for Singaporeans, especially young couples who are trying to buy their first home. The most prominent benefit that people are after is affordability. Government subsidies in the form of housing grants significantly lower both the upfront cost and monthly instalments of these homes. On top of that, buyers can rely on housing loans and CPF funds to ease the financial burden even more.

As the name suggests, BTO flats come brand new. So, you won't have to worry about unexpected breakdowns or repairs since the appliances are still new. You might need to renovate the place a bit to fully transform it into a home, but overall, BTO offers a convenient fresh start.

BTO Considerations

BTO makes a good starter home, a stepping stone perhaps. However, it is also a long-term commitment. The building process itself takes around 4 years, and then there's the Minimum Occupation Period (MOP) of 5 years - that's a total of 9 years before you can even consider selling or upgrading.

While staying put allows you to accumulate your CPF funds for future purchases, some people might find this long timeframe inconvenient, especially since opportunities can come and go and so much can change in 9 years. So, not everyone loves BTO. My colleague actually regrets getting one. You can read his story and experience with BTO here.

If you are looking to invest, you might be better off exploring other options. Upgrading to a more expensive property sooner can accelerate wealth accumulation through capital appreciation. This will put you in a stronger financial position down the road.

BTO Process

Check your eligibility

Before you do anything, you should apply for an HDB Flat Eligibility (HFE) letter, which will inform you of your eligibility to buy an HDB flat, receive CPF housing grants and take up an HDB housing loan. It's an upfront application that will take about 21 working days or around one calendar month. This may take longer during peak season when HDB launches the sales. Make sure to plan accordingly and do this early because you must have a valid HFE letter when you apply for a flat in HDB's sales launches.

There are two steps to the HFE letter application: preliminary HFE Check and the actual HFE Letter Application.

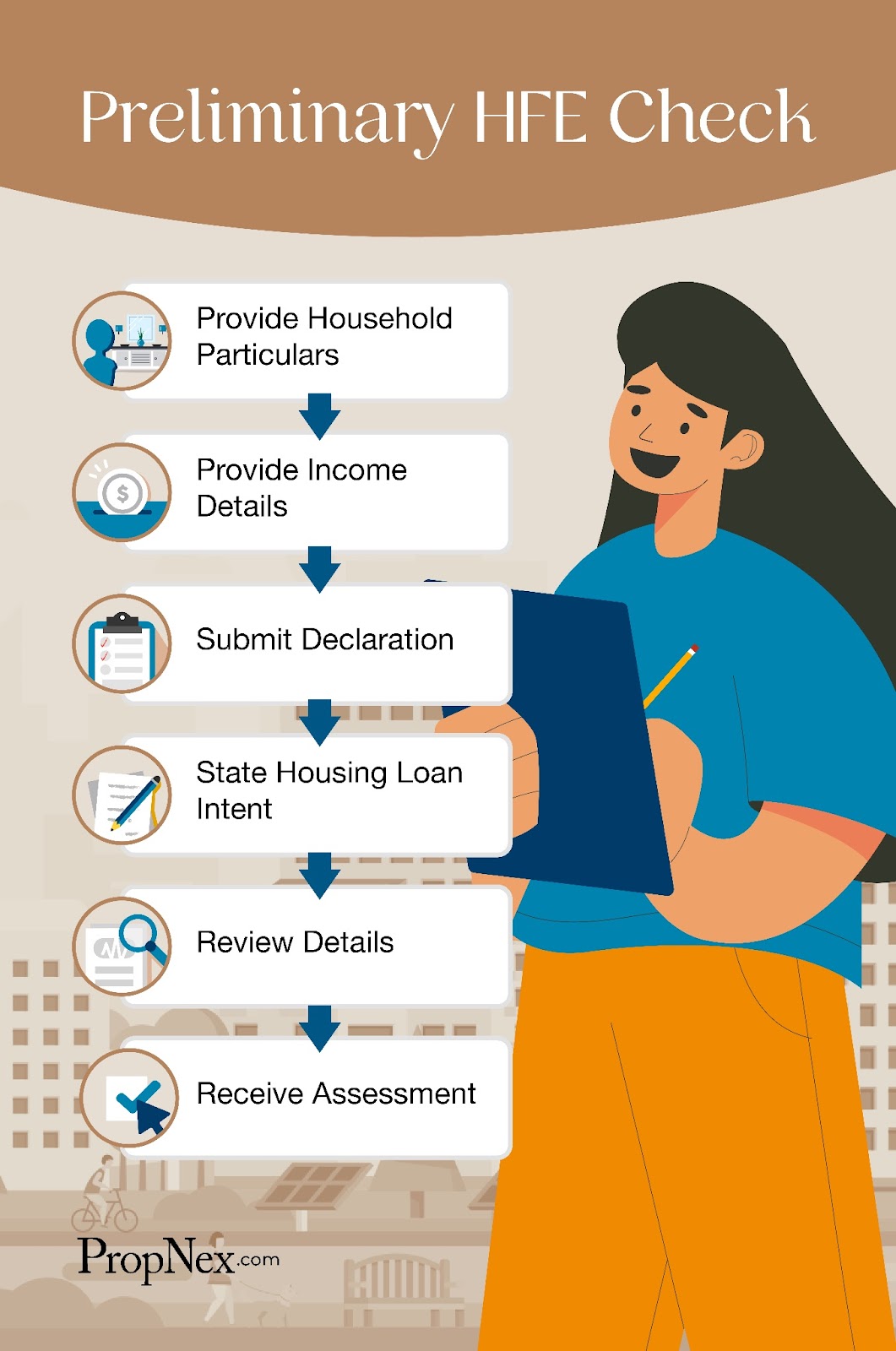

Preliminary HFE Check

The preliminary HFE Check is a quick questionnaire that only takes around 10 minutes to complete. Simply log in on HDB's portal with your Singpass and fill out the form. It's important that you provide accurate information during this step because the assessment will be based on your declaration. Pro tip: Have your Singpass login information and personal details (of all applicants and occupiers) ready beforehand.

After completing the preliminary check, you will receive a quick overview of your household's eligibility for your advance planning. If you are still interested in buying a flat after receiving your preliminary assessment, you may proceed to the next step to obtain a confirmed assessment.

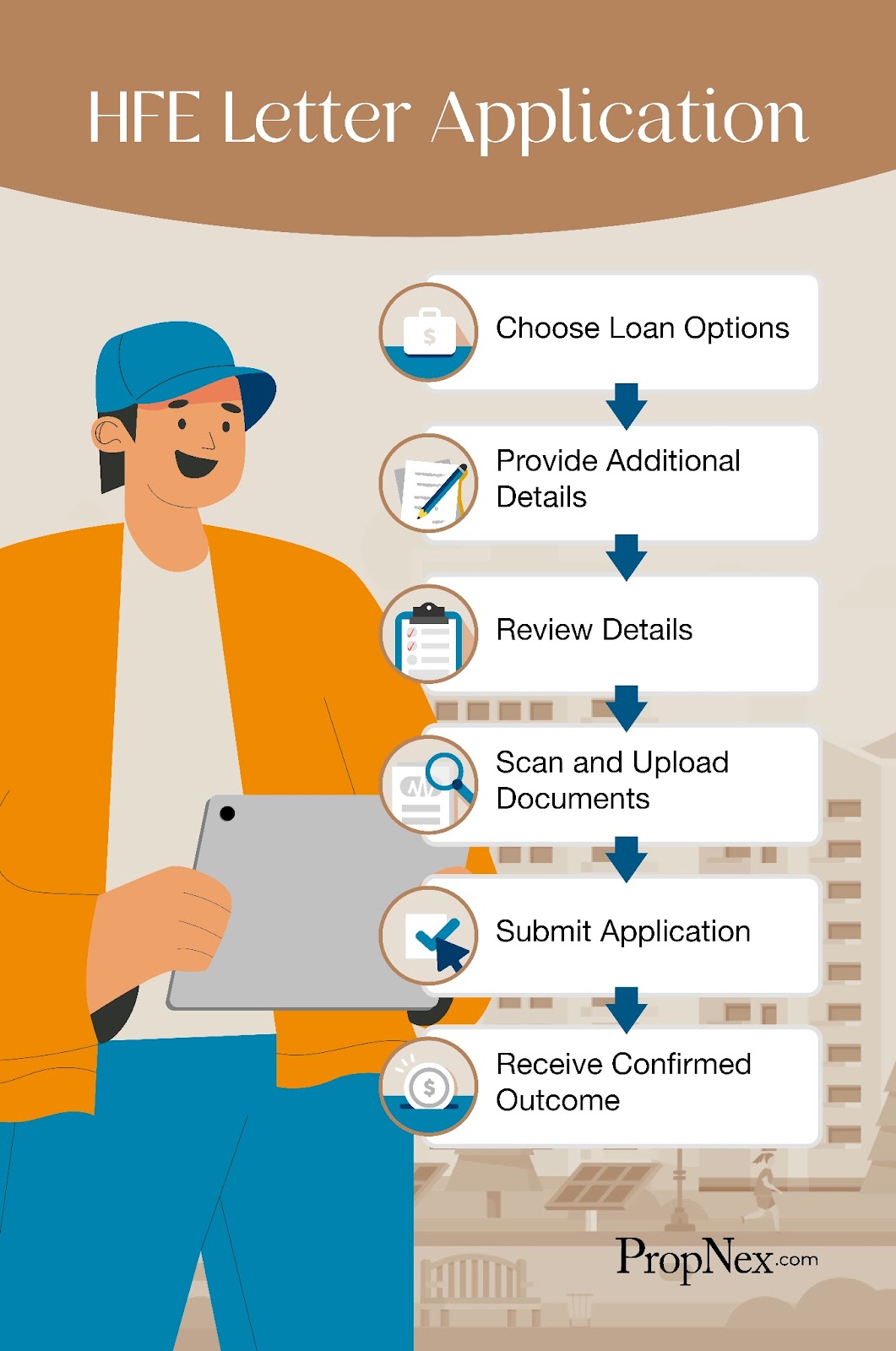

HFE Letter Application

Once you are ready to buy a flat, apply for an HFE letter within 30 calendar days from the date you initiated the preliminary check. If you don't apply within the time limit, your preliminary assessment will expire and you will have to start over. Additionally, you should prepare any supporting documents that you might need for the application such as proof of income and marriage certificates.

If your application is approved, congrats! This is a significant step towards your home ownership journey. Your HFE letter is valid for nine months from the date of issue. To maintain its validity during this period, make sure there are no significant changes to your household's income or financial situation. Furthermore, the applicants and occupiers listed in your application should remain the same.

If your application is rejected, HDB will typically provide the reason. This can be about your household's income ceiling, ownership of other properties, citizenship or residency status, outstanding debts and/or unresolved issues with previous HDB transactions. You can then address the issue and reapply for the HFE letter. However, if you believe that the rejection was made in error, you can appeal the decision to HDB and provide supporting documents as evidence.

Apply for a flat

With an HFE letter ready, the next thing you need to do is to apply for a flat online during HDB's sales launch. HDB launches new BTO projects several times a year and applications are typically open for a week during each launch. So, watch out for these launches and apply as soon as you can.

Balloting

Due to high demand, HDB uses a balloting system to determine who gets to choose a flat first. This computerised system assigns a random queue number to each eligible application. Results are usually available within two months after the application period has closed but it will also depend on the sales launch and flat supply.

If successful in the ballot, you'll be invited to select and book a flat based on your queue position. The lower your queue number, the earlier you get to select your preferred flat (from the remaining availability). There are also certain schemes that can increase your chances of receiving a favourable queue number. Read more about them here.

Booking a Flat

If you are shortlisted for a flat, you can continue your application even if your HFE letter is expired. HDB will notify you of your flat booking appointment two weeks in advance. You can view this invitation, which will include the list of available flats and needed documents, on My HDBPage. It's important that you attend the appointment in person. However, if you are unable to do so, you can authorise a representative.

The booking process requires you to pay an option fee, which varies depending on the flat type you select. Below are the details

| Flat Type | Option Fee |

| 4-room and bigger | $2,000 |

| 3-room | $1,000 |

| 2-room Flexi | $500 |

To ensure the booking process goes smoothly, submit all the required documents through MyDoc@HDB before the flat booking appointment. Here are the everything you need to prepare:

- Identity cards (IC) of all listed applicants/occupiers (you may need to log on to the Singpass app to verify your digital IC)

- Passports of non-resident occupiers (if any)

- Your child(ren)'s birth certificate (if any)

- Marriage certificate (if you are married)

- Divorce certificate (if you are divorced)

- Death certificate of spouse (if your spouse is deceased)

- Your birth certificate and your parents' marriage certificate (if you are buying a flat under the Multi-Generation Priority Scheme or Married Child Priority Scheme)

- Doctor's certification of pregnancy or your child's birth certificate (if you are buying a flat under the Parenthood Priority Scheme)

During the booking, buyers are also offered the Optional Component Scheme (OCS), which lets you add features like flooring, internal doors and sanitary fittings to your new flat. These features will be installed before you collect your keys, saving you some time and effort. If you decide to skip the OCS during your booking, you won't be able to add them later. So decide wisely during your appointment. You should also note that this added convenience is not applicable to projects built using the Prefabricated Prefinished Volumetric Construction method as these flats already come equipped with these features.

Financing and Mortgage

Once you select a flat unit, you'll need to arrange a financial plan to purchase the property. Most buyers rely on housing loans provided by financial institutions like banks or HDB. If you choose to do this, you need to request a Letter of Offer to confirm the housing loan. But before committing to anything, you should compare loan packages and calculate your borrowing capacity. Learn more about debt ratios and get budgeting tips here.

Agreement for Lease (AFL)

Once financing is secured, you'll need to sign the AFL, which outlines the terms and conditions of the flat purchase. This includes lease tenure, payment schedule, as well as the rights and responsibilities of buyer(s) and HDB. If you booked an uncompleted flat, you'll be invited to sign the AFL within nine months. If you booked a completed flat, the process could be faster, within six to nine months. During this step, you are also required to pay the initial down payment, stamp duty and legal fee.

Completion and Key Collection

After your flat is completed, you will need to pay a survey fee and HDB will conduct a final inspection to ensure that the flat meets the quality standards. If the results are satisfactory, HDB will notify you about the key collection date, when you will receive the keys to your new home. But before you can collect the keys, you must pay the balance purchase price in full. Then voil! You're a homeowner ready to move in.

Cancellation

Take the time to do your research and make sure you are fully prepared before applying for a flat because cancelling your BTO application may incur monetary penalties and add challenges to your future application. Below are the details.

| Stage of Application | Financial forfeiture | Consequences |

| During sales launch | None | No penalty |

| After sales launch but before booking a flat | None | If you were invited to book a flat but choose not to even though there are units available, you will incur a non-selection count.

For first-timer families, a non-selection count means you will be considered a second-timer for one year. If you incur another non-selection count during this period, your first-timer priority will be further suspended for another year. Additionally, any additional ballot chances accumulated from previous applications will be reset to zero.

For first-timer singles and second-timer families, a non-selection count means you won't be able to participate in any sales launches for a year.

In situations where there are only 10 or fewer BTO flats to choose from, HDB can waive non-selection count. |

| After booking a flat but before signing the agreement for lease | Option Fee | You must wait one year from the date of cancellation before you may apply or be included as an essential occupier for:

For first-timer families, any additional ballot chances accumulated from previous applications will be reset to zero. |

| After signing the agreement for lease but before key collection | 5% of the purchase price |

Now that you are prepared for every step, you are more than ready to #BTOgether. However, if you feel reluctant to prepare everything on your own, you can always come to us for some guidance and help!

You should also remember that BTO is not the only option available. Though its affordability makes it an undeniably popular choice among young couples, BTO can be a lengthy process you might prefer to avoid. There are also different paths that may be more suitable for your needs and lifestyle. Resale flats, ECs and private properties have perks that you won't want to miss out on. We'll uncover them another time, so stay tuned!

Related articles: Resale HDB Flats Vs New BTO, Which Should You Choose?, Game of Luck: A Crazy Little Thing Called BTO, Lunar New Year And BTO Launch Weighed on HDB Resale Market in February

Views expressed in this article belong to the writer(s) and do not reflect PropNex's position.