博纳精选

August 29, 2024

10 Essential Tips When Utilising Your CPF for Home Purchases

Daryl Wee

Senior Content Writer

In Singapore, buying a home is a significant financial commitment, and the majority of us definitely tap into our Central Provident Fund (CPF) to make this process more manageable. The CPF scheme is a mandatory social security saving plan which aims to support retirement, healthcare and also home ownership. Understanding how to use these funds for purchasing property is crucial. Here are nine key points to consider when using your CPF for buying a house:

The CPF Ordinary Account (OA) is a critical component when it comes to home financing. Contributions to the OA can be used for housing, education, investment, and insurance. This account accumulates savings that earn an interest rate of 2.5% per annum, which can be utilised for purchasing a property. This rate has been steady since its inception, regardless of the fluctuation of the commercial banking rates.

Maybe because it is ingrained in us through our parents to get a BTO as our first home and settle down for the rest of our lives, many seem to be shocked when they realise that the monies in CPF can actually be utilised even for private homes, and even in some cases, commercial and industrial properties. You can use it to pay for your monthly mortgages, and also downpayment to a certain extent.

Before utilising your CPF savings for property purchases, you must meet certain eligibility requirements. These include age, citizenship, and the type of property. For instance, you must be at least 21 years old to use your CPF savings and purchase a property in Singapore. But don't worry, you won't even be able to own a property by the age of 21, so this probably makes sense too.

CPF housing grants can significantly reduce the financial burden of buying a home. These grants are available for both HDB flats and Executive Condominiums (ECs). First-time buyers and families often benefit from grants like the Enhanced CPF Housing Grant (EHG), which is based on household income and other criteria. Sad to say, private home buyers are not entitled to such grants. For more on grants & schemes, we got you covered here.

When using CPF funds for property, it's crucial to understand the concepts of Valuation Limit (VL) and Withdrawal Limit (WL). The VL is the lower of the purchase price or the market value of the property at the time of purchase. The WL is set at 120% of the VL. Beyond this limit, you cannot use your CPF funds unless you have sufficient savings in your Retirement Account (RA).

Also, another important thing to note is that the retirement sum requirements change on a yearly basis to ensure that it keeps up with rising cost, it is better to check the current rates directly on CPF's website.

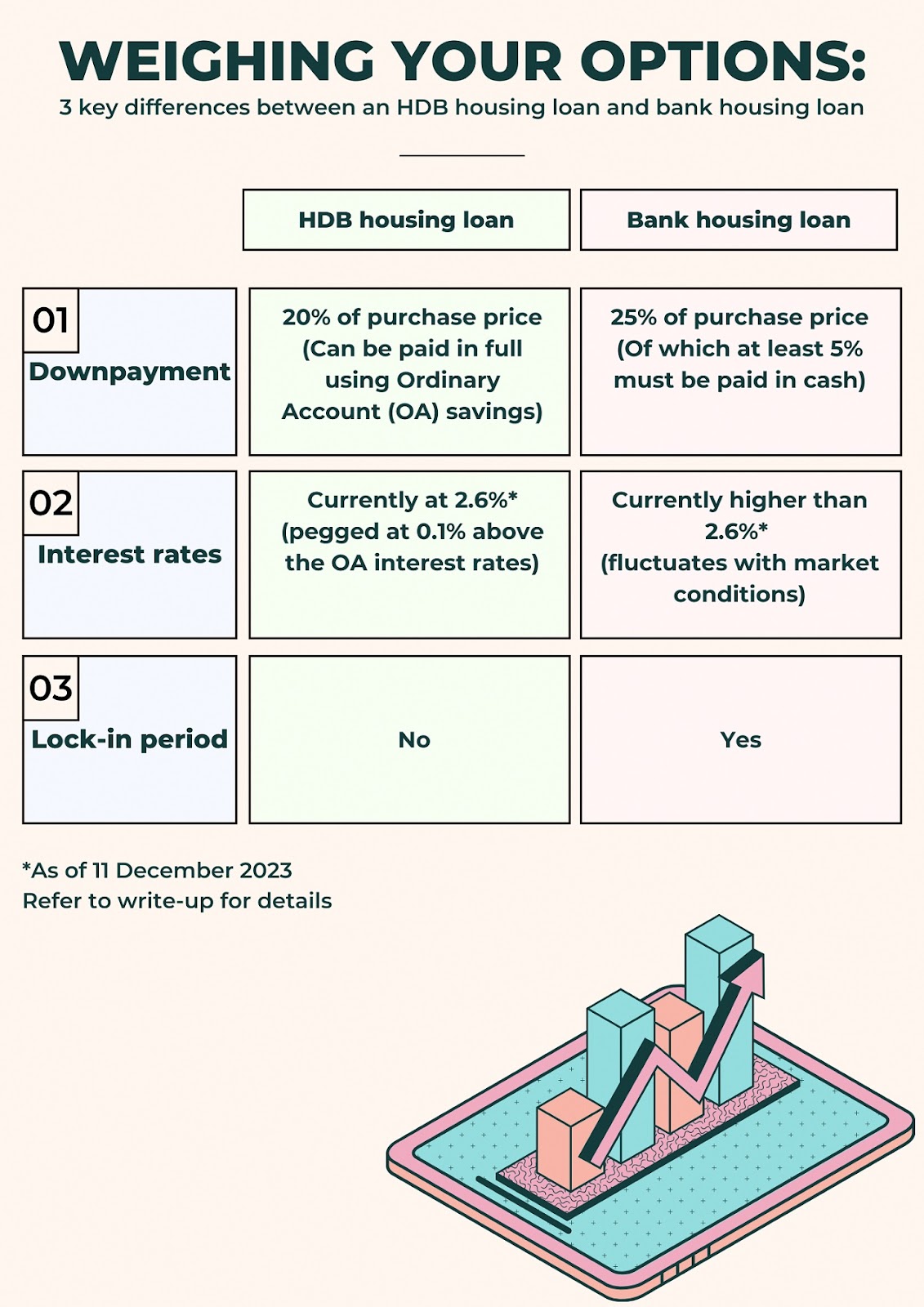

Depending on whether you are making your home purchase using a bank loan or HDB loan, it makes a difference in terms of the utilisation of your CPF monies.

Source: CPF

CPF savings can also be used to service monthly mortgage repayments. This applies to both HDB loans and bank loans. However, it's important to ensure that your monthly CPF contributions are sufficient to cover the mortgage payments to avoid dipping into your cash reserves.

The Home Protection Scheme (HPS) is an essential insurance plan that protects CPF members and their families from losing their homes in the event of permanent incapacity or death. This scheme is mandatory for those using CPF savings to repay their HDB loans. It ensures that your outstanding home loan is covered, providing peace of mind.

Refinancing your home loan with CPF funds is possible, but it comes with specific conditions. For instance, when refinancing from a bank loan to an HDB loan, you must ensure that your CPF savings are adequate to cover the new loan amount. Additionally, refinancing should be carefully considered to ensure it aligns with your long-term financial goals. For such intricate planning, you should always speak to an expert to understand what you are getting yourself into.

Upon selling your property, you are required to refund the CPF monies used for the purchase, including the accrued interest, back to your CPF account. This ensures that your CPF savings are replenished for future needs, such as retirement. Hopefully, upon returning the amount used for your home purchase with accrued interest, you will still be able to have cash profits. Many are not unaware of accrued interest and how it works, resulting in miscalculation. Perhaps I should do a separate article addressing this, what do you think? Yay Nay?

Lastly, if you didn't know, common stamp duties such as Buyer's Stamp Duty and Additional Buyer's Stamp Duty can be paid using your CPF account. Only the monies in the OA can be used to pay off these stamp duties. One more thing to note, if you are purchasing a fully completed home, the stamp duties have to be paid in cash within 14 days of concluding your property purchase.

Conclusion

I hope that these 10 points will help you in terms of understanding how you can utilise your CPF to aid you in your housing journey. By comprehensively grasping the nuances of CPF usage, eligibility criteria, housing grants, and repayment obligations, you can make well-informed decisions that support both your immediate housing needs and long-term financial plans. Always consider seeking advice from professionals before you make any crucial housing decisions.

Views expressed in this article belong to the writer(s) and do not reflect PropNex's position.