Rentvesting Revealed: The Key To Your Property Dreams

There are two ways to approach when looking for a home in the Singapore property market: buying or renting. Even after determining which direction you are going, there are additional factors to consider, such as whether you are going for a BTO or condo, or even which region you are considering living in.

That being said, like most Singaporean households, we have been instilled in us the mindset of homeownership. Most would prefer owning a house as compared to renting. However, as the real estate market continues to rise, Singaporeans are looking for unique ways to boost their affordability.

Recently, I came across the term rentvesting. Popularised in New Zealand and Australia, it is an investment strategy in which homeowners rent a property to live in, while renting out their bought home as an investment property. This strategy is particularly beneficial for homeowners who own properties in prime areas where housing prices are significantly higher. As such, many rent them out to professionals working in those areas while they themselves rent in suburbs where housing prices are more affordable.

As I read this, it got me to consider its possibility in Singapore. Singapore's property market is incredibly competitive, with many foreign investors drawn to it. Now, there are some regulations set in place to maintain its stability. If you currently own a private property, you are now allowed to own a HDB concurrently. Additionally, there is a 15-month wait-out period should you be looking to move to a resale HDB.

On the other hand, HDB homeowners can own private properties. However, they can only do so after fulfilling their MOP. Singapore homeowners who have an HDB apartment and are purchasing a condo, will be subjected to 20% ABSD. Now, if you are a private homeowner looking to get another private property, you can do so as long as you are able to afford the price tag and the ABSD.

So, back to the question: Would rentvesting be the ideal solution for HDB homeowners looking to upgrade?

It might not seem logical to most to be paying off rent and home mortgages concurrently. While there is no one correct answer to the question, it all depends on your lifestyle, life stage, and budget. Rentvesting offers the best of both worlds. If you are already living in a HDB apartment, you can rent out the entire apartment to at most eight people (only after your MOP) to cover your remaining mortgage. If you are able to earn a profit from your rental income, you may even use some of that to cover part of your own rental expenses.

Let us take a look at a hypothetical scenario.

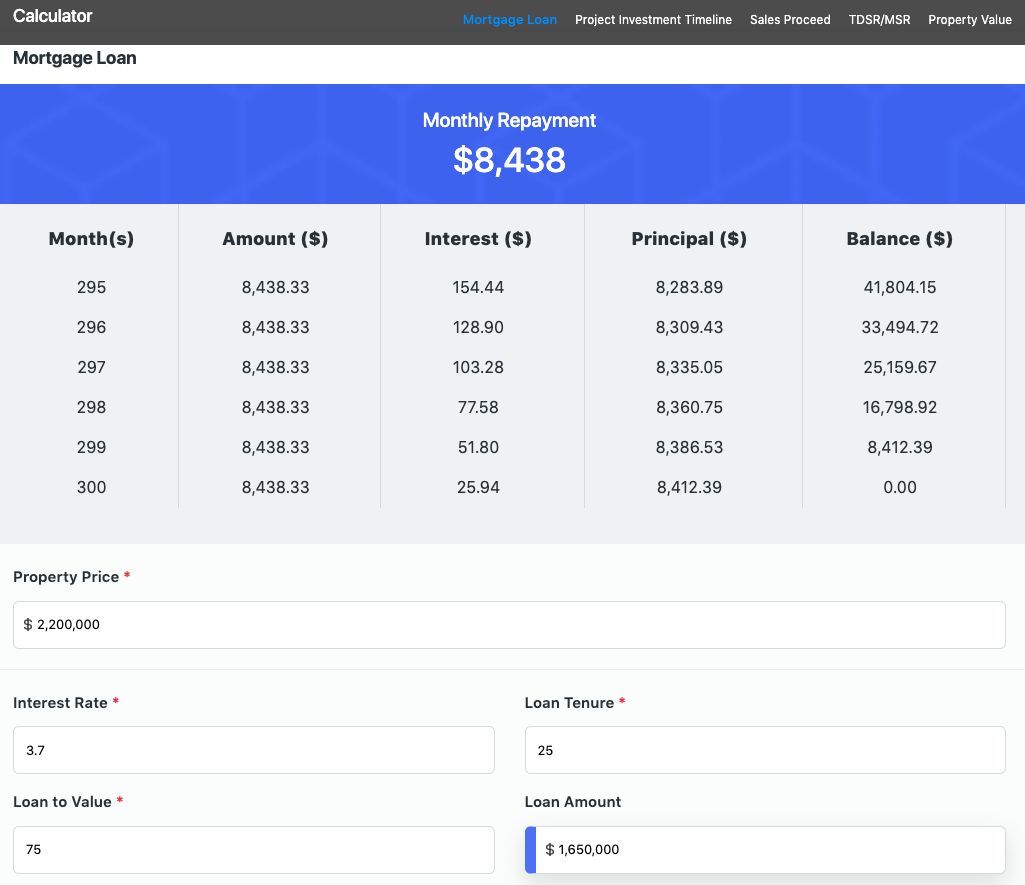

A family of four living in a 4-room HDB apartment along Bishan St 23 is looking to upgrade to a condo in the same area as they want access to facilities, such as swimming pools, BBQ pits, and gyms, where they can host their friends and family. If they decide to sell their apartment, they would be glad to know that the highest recorded transaction at the time of writing was approximately $988,889. A condo project within Bishan can be rather expensive since it is located in the RCR. Just a 15-minute walk from where their HDB apartment is Sky Vue, a 99-year leasehold condo development. A 3-bedroom unit would best fit their family size. However, it would cost them about $1,900,000 to $2,500,000.

Using PropNex's online calculator, here is the monthly repayment of their condo mortgage loan. At the time of writing (10 Oct 2024), the lowest private mortgage loan is Citi's at a floating rate of 3.7%. Here is the monthly repayment of their HDB mortgage loan if they take it

Now, what would it look like if the family decides to rentvest?

Assuming they have fulfilled their MOP and decided to rent it out, they would be glad to know that the highest recorded rent was $4,400. The most recent rental cost of a 3-bedroom unit at Sky Vue is $6,100.

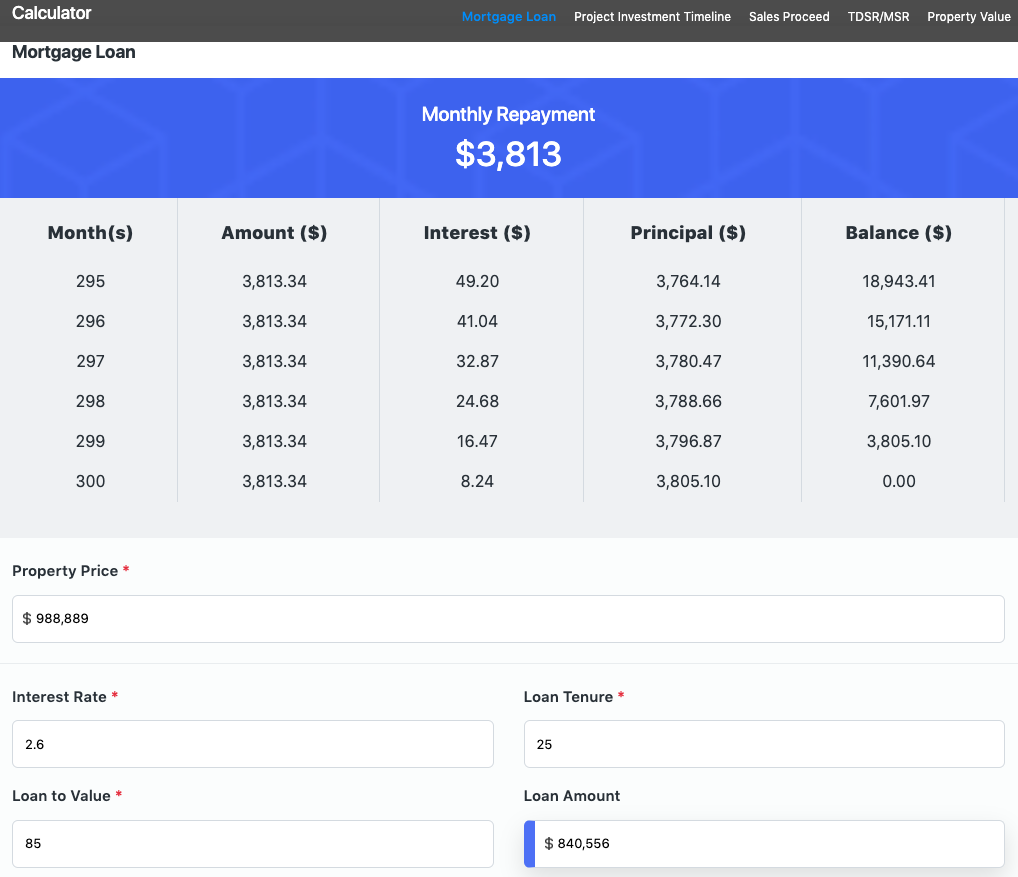

Here is the monthly repayment of their HDB mortgage loan if they take the HDB loan:

HDB's housing loan has a lower cash &/or CPF downpayment requirement but a higher LTV of 85%. That being said, there are several requirements that you need to meet to qualify for an HDB loan, such as not exceeding the maximum household income cap and not owning any commercial or private properties under your name.

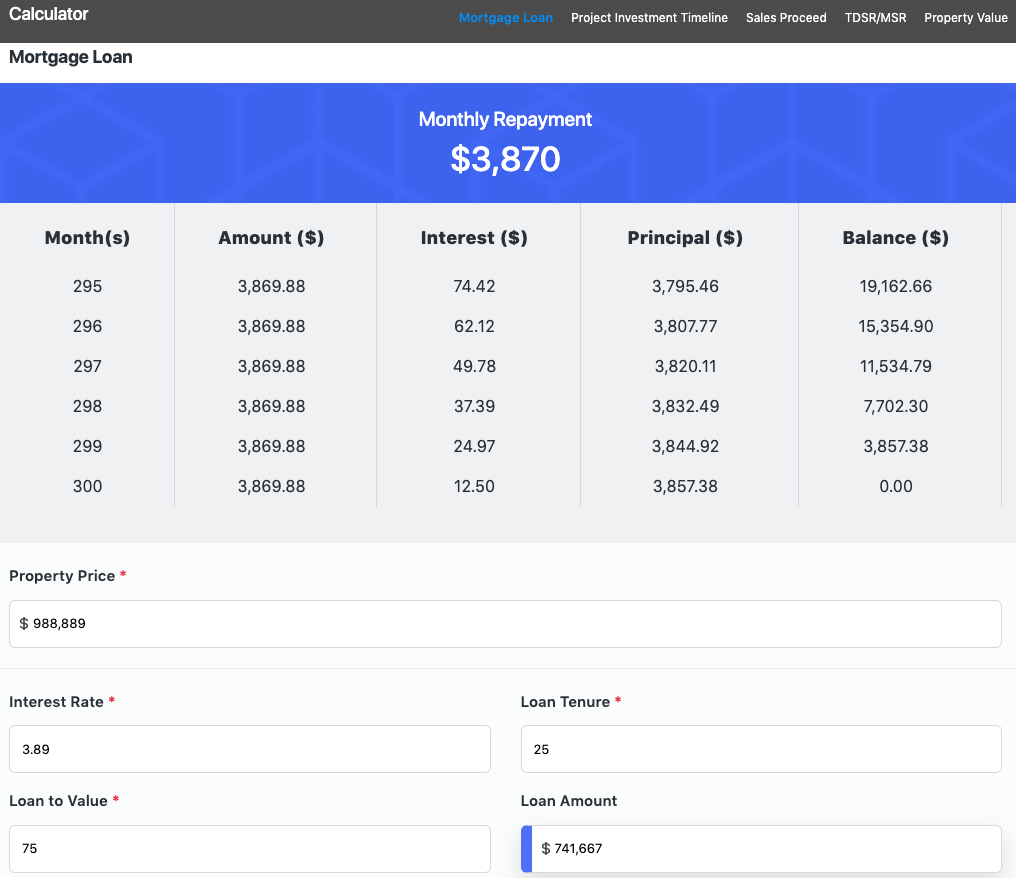

At the time of writing (10 Oct 2024), the lowest HDB mortgage loan is HSBC's at a floating rate of 3.89%. Here is the monthly repayment of their HDB mortgage loan if they take it:

A bank loan has a minimum 5% cash downpayment requirement but a lower LTV of 75%. Taking a bank loan could potentially appear more attractive as different banks offer varying interest rates and package options. As such, take your time to choose the best package that you can afford. When assessing which type of loan is right for you, consider:

- If there is any free conversion at the end of or within the lock-in period

- If there is any waiver of redemption payable should the property be sold during the lock-in period

- The duration of the lock-in period

- If a floating or fixed interest rate is preferable for you

Whether bank or HDB mortgage loan, you will need to consider your risk profile and financial capabilities.

HDB's mortgage loan with a fixed rate of 2.6% is ideal for those seeking stability and lower financial risk. With this loan, you benefit from the predictability of fixed monthly repayments, as the interest rate remains constant over the life of the loan, offering peace of mind amidst fluctuating market conditions. The consistency of HDB's loan also makes it easier to plan and manage your long-term financial commitments, reducing the stress of dealing with changing interest rates. Furthermore, the 2.6% interest rate is pegged to the CPF Ordinary Account interest rate plus 0.1%, providing a certain level of stability since CPF interest rates tend to be less volatile compared to bank rates.

If you are open to taking on some financial risks and possess the discipline to actively manage your finances, opting for a bank loan may be a viable choice. To ensure you are getting the best deal available, you need to monitor and refinance regularly, typically every few years. While bank loans can provide cost savings in the short term, interest rates are subjected to market fluctuations, which may lead to higher monthly repayments over time. That being said, the recent lowered Federal Reserve interest rates may be the time to consider a bank loan.

Nevertheless, a $988,889 4-room HDB would set them a monthly mortgage of $3,813. If they are able to rent out the entire HDB at $4,400, they still can profit $587, which can go to cover their $6,100 monthly rent at Sky Vue. This means they are essentially only spending $5,513 on monthly rent, which is significantly more affordable than the monthly mortgage ($8,438) they have to fork out if they were to purchase a condo unit. If they were to rent out their HDB according to individual rooms, they might even be able to earn more rental income than renting out the entire apartment.

Long gone is traditional homeownership where you either buy or rent. Why not combine the best of both worlds to optimise your investment opportunities? Rentvest enables homeowners the capability to build up their financial portfolio without mortgaging themselves to the hilt.

So, back to the question: To rentvest or not to rentvest? The answer depends on what makes sense for your financial needs and circumstances. However, like any property-related decisions, whether it is investing, renting, or purchasing, it is vital that you have adequate resources to do so. If you are a Singaporean homeowner who already owns a property and is looking to upgrade, this strategy might be worth considering.

Views expressed in this article belong to the writer(s) and do not reflect PropNex's position. No part of this content may be reproduced, distributed, transmitted, displayed, published, or broadcast in any form or by any means without the prior written consent of PropNex.

For permission to use, reproduce, or distribute any content, please contact the Corporate Communications department. PropNex reserves the right to modify or update this disclaimer at any time without prior notice.

Oh no!

Enjoy our Content?

If it is of any consolation, know that you are not alone in this real estate journey. Let us show you the way to make this journey an interesting and enjoyable one!

Suggested Reads

Upcoming Events

View more

You may like

When 8 Is Worth More Than 4: How Number Superstitions Shape Property Decisions

July 14, 2026

Cold Prospecting for Real Estate Agents: Making First Contact More Relevant

July 13, 2026

Prospecting Discipline: Building Daily Habits That Create Future Appointments

July 13, 2026

Warm Market Prospecting: Starting Conversations Without Damaging Relationships

July 13, 2026

Listing Presentation: Winning Seller Confidence Before the First Viewing

July 10, 2026

Rejection Follow-Up: When to Nurture, When to Pause and When to Move On

July 10, 2026