From market signals to financing strategies and upgrading decisions, explore curated learning to help you buy, sell, or invest with clarity and confidence.

From market signals to financing strategies and upgrading decisions, explore curated learning to help you buy, sell, or invest with clarity and confidence.

Recent Hot Topics Singaporeans Care About

How We Help You Learn

Our education ecosystem spans seminars, articles, market insights, tools, and data-driven frameworks to help every homeowner and investor make smarter decisions.

Start with our latest guides, insights, and explainers. Updated regularly to help you decode the Singapore property market.

Curated Content Just For You to Stay Ahead

Bank Of Mum & Dad 2: How To Help Your Child Buy A Home Without Risking Your Future

Every Sunday, the Lims have dinner at the same table their three children grew up doing homework on. Tonight, the topic is Charmaine's upcoming resale flat purchase, and her parents, Wei Ming and Yvonne, have offered to top up her downpayment.Nobody at that table is asking whether to help. They've already decided.What nobody has asked yet is how.That's the gap this article sits in. Once the emotional question of whether to help has been answered, a second question begins: how should the help actually be structured?And that second question matters more than many families realise. The mechanics of a gift, loan, CPF usage, bank checks, and family documentation are where good intentions can become complicated, years after the cheque has cleared. TL;DR Helping your child buy a home may feel straightforward, but the biggest risks often have nothing to do with the property itself. The way the money is structured today can affect family relationships, future inheritance, and even what happens if circumstances change years later. Gift or loan is the first fork, and it's bigger than it looks: A gift is simple and final. A loan can make fairness between siblings easier to manage, and can be documented, adjusted, or forgiven later - but only if it is put in writing from day one. The scenario nobody plans for is the one worth planning for: If your child's marriage does not work out, how the money was given - and how it was used - may affect whether it is protected from division as a matrimonial asset. The paperwork becomes important once real money moves: Singapore banks apply anti-money-laundering checks to large or unusual fund transfers, so an undocumented lump sum can slow down - or complicate - your child's own mortgage approval. Help your child without compromising your own runway: Model what the gift or loan does to your own retirement and housing plans before you commit to a number. Fairness among siblings is easier to manage early than late: A quiet loan or gift to one child, if it stays quiet, tends to surface at the worst possible time - usually when a will is being read. Bottom line: The money is usually the easy part. The harder question is how to structure it in a way that protects your child, your retirement, and family harmony long after the property purchase is completed. In this article, we will explore: Gift or loan - the fork that shapes everything The conversation nobody wants to have - but should How the gift actually moves through the bank - CPF and loan mechanics Before you write the cheque - what it does to your own plan One child now, one child later - keeping it fair The paperwork checklist Gift or loan - the fork that shapes everything else Every other decision in this article follows from this one.A gift is clean. There's no repayment schedule, no interest, no awkward conversation five years from now about when the money is due back. For many families, that simplicity is exactly the point - the whole reason for helping is to remove pressure from a child's life, not add a new obligation to it.But a gift is also permanent and, once given, may be difficult to reverse or rebalance. It has effectively moved out of your hands. It cannot easily be adjusted if your own circumstances change, or if a sibling needs similar help later.A loan does the opposite. It keeps the money notionally on your side of the ledger, which matters if you have more than one child and want to keep things even. It can be renegotiated, partially forgiven, or extended. And - this is the part families often miss - a loan that is properly documented may carry more weight in a family dispute or divorce than a gift, precisely because it was not intended to be a gift.The catch is that a loan only works as a loan if it looks like one on paper. A verbal understanding between parent and child may be harder to prove later, especially if a bank, lawyer, or court needs to understand what the transfer was meant to be. Without a note, repayment terms, or any record of repayment, an informal family loan can start to look like an undocumented transfer of money.If the family wants the arrangement to be treated as a loan rather than a gift, the intention should be documented clearly, preferably with legal advice, even between people who trust each other completely.A simple family loan document does not need to be a bank-grade facility agreement. At minimum, it should set out the amount, whether interest applies, the expected repayment schedule, even if it is flexible, and what happens if the child sells the property before the loan is repaid. Have it signed and dated by both parties, and keep a copy.It is a modest amount of effort for something that only matters if things go wrong - which is exactly when you'll be glad it exists.The conversation nobody wants to have - but should Here's the section most guides skip, and it's the one that matters most.If your child's marriage ends in divorce, what happens to the money you gave or lent them?Under Singapore's Women's Charter, assets a spouse receives by gift or inheritance from a third party - including a parent - are generally excluded from the pool of matrimonial assets that gets divided on divorce. That's the starting point, and it is good news if you're the one who gave the money.But there are important exceptions, and they are easy to trip over without realising it.The first is the matrimonial home itself. Property that the couple actually lived in together is treated differently from other gifted or inherited assets. It can be drawn into the matrimonial pool even if the funds that helped buy it originated as a gift from a parent. In practice, this means a cash gift that goes straight into buying the home your child and their spouse live in may not carry the same protection as, say, gifted shares or a gifted investment portfolio kept separately.The second is how the money was treated after it was given. Courts may look beyond the label on a transaction to consider intention, conduct, and the surrounding evidence. If gifted funds are mixed into joint accounts, used to pay shared household expenses, or referred to by either spouse in writing as "our money" rather than "my money", that may affect how the gift is viewed later.Even casual messages can matter. In one Singapore Court of Appeal case, correspondence including WhatsApp messages was considered when assessing how the parties treated certain assets. The point is not that every family message will become evidence one day. The point is that protecting a gift is not only about what was intended at the start - it is also about how the money is handled, described, and used afterwards.None of this is a reason not to help. It is a reason to think about how.If preserving the money's separate status matters to your family, structuring it as a documented loan - rather than a gift folded into joint finances - may give your child something clearer to point to later, if they ever need to. A deed of gift, if you go that route, is also worth having drafted properly rather than assumed from a bank transfer with no paper trail at all.This is not a conversation anyone enjoys having before a wedding, or even before a home purchase. But the families who have it early are the ones who avoid a much harder conversation later.How the gift actually moves through the bank - CPF and loan mechanics Once you've settled gift-versus-loan, the money still has to pass through the system, and a few mechanical points are worth knowing before it does.Large or unusual deposits get noticed. Singapore banks are required to apply anti-money-laundering checks to significant fund transfers as part of standard due diligence. A large lump sum landing in your child's account shortly before a property purchase may trigger a request for more information - where the money came from, and whether it is a gift or a loan. This is not a reason to avoid helping; it is a reason to be upfront about it from the start rather than have it surface as a hold-up during mortgage processing.CPF changes the cash picture, but not the need for proper planning. Your child's CPF Ordinary Account savings may be used to fund part of the property purchase, subject to CPF rules, valuation limits, and the type of property being bought. This is why two buyers with the same income and the same purchase price may still have very different cash shortfalls - one may have more CPF OA savings available, while another may need more cash upfront.A parental gift or loan usually comes in to bridge this gap. It may help with the cash portion of the downpayment, the balance not covered by CPF, stamp duties, renovation costs, or the liquidity buffer after purchase. But it should not be treated as a substitute for understanding the full funding structure. Before the money moves, your child should be clear on how much of the purchase is funded by CPF, how much requires cash, how much is covered by the housing loan, and what reserves remain after completion.It affects how much your child can borrow, not just how much they can put down. Loan eligibility in Singapore is governed by the Total Debt Servicing Ratio, capped at 55% of gross monthly income across all property loans, and, for HDB flats and executive condominiums bought from developers, the Mortgage Servicing Ratio, capped at 30%. A cash gift used purely for the downpayment does not change your child's income for these calculations. But if the loan option is used instead, and it is structured as a formal, repayable loan with documented instalments, it could be treated as a debt obligation that affects their TDSR.This is one more reason the gift-versus-loan decision is not just about family dynamics. It may have a direct bearing on how much your child can actually borrow.Loan-to-value limits still set the floor on what needs to be funded another way. For a first HDB housing loan, the LTV limit currently stands at 75%, meaning at least 25% of the purchase price has to come from cash, CPF, grants where applicable, or other approved funding sources. For a first bank loan on a private property, LTV can go up to 75% if the loan tenure is 30 years or less and the borrower is under 65 by the end of the loan term, subject to bank assessment and prevailing rules. Otherwise, the limit may be lower.A parental gift or loan is most commonly used to help cover the shortfall - the downpayment gap that CPF savings and the loan itself do not fully reach - rather than the mortgage instalments themselves.Keep the money separately traceable, at least initially. Whichever structure you choose, avoid having the gift or loan arrive as an unexplained cash deposit. A bank transfer, ideally accompanied by a short note stating what it is for, creates a paper trail that protects everyone - the donor, the recipient, and the transaction itself - if any of these figures matter later, whether for a bank's underwriting process or a future family or legal conversation. Enjoying our insights so far? Stay updated with the latest property trends, expert analysis, and market perspectives from PropNex. Join our mailing list Before you write the cheque - what it does to your own plan This is the section parents skip most often, usually because the whole point of the exercise is to think about their child, not themselves.But the most protective thing you can do for your family is make sure the help you're giving does not quietly undermine your own retirement.Before committing to a figure, it is worth modelling three things.First, what this withdrawal or gift does to your own CPF balances, cash savings, and retirement sum, particularly if the money is coming out of savings earmarked for your own housing or retirement needs.Second, whether your own home still fits your life for the next 10 to 20 years, or whether the timeline for right-sizing needs to move up because a chunk of your liquidity has gone toward your child's purchase instead.Third, what buffer you're left with for the unpredictable costs of ageing - healthcare in particular - after the gift or loan is made.None of this means parents should not help. It means the number should come from a plan, not from a feeling of what seems reasonable in the moment. Families who have gone through the exercise of right-sizing their own home often find this a natural place to revisit that thinking.If freeing up equity from your own property is part of how you would fund helping a child, it is worth reading that decision through the same lens as your retirement plan, not as a separate, disconnected choice.In other words, the child's purchase should not be planned in isolation. The better question is whether the family's overall property position still works after the help is given - the parent's home, the child's home, available cash, CPF, future healthcare needs, and the option to right-size later. A loving gesture is strongest when it protects both generations.One child now, one child later - keeping it fair If you have more than one child, this is the question that eventually gets asked, even if nobody asks it out loud at first:What happens for the others?Helping one child buy a home while another is still renting, still saving, or simply not at that stage of life yet, is not unfair on its own. Timing differs, and needs differ. What creates friction later is not the help itself - it is silence about it.Families who handle this well tend to do one of three things.Some keep a simple record of what has been given to each child, with the intention of adjusting inheritances later so the ledger balances out. Some structure the help as a loan specifically so it can be forgiven equally, or repaid and redistributed, when the time comes. And some simply talk about it - telling all their children, not just the one receiving help, what is being given and why.The version to avoid is the one where a sibling only finds out about a six-figure gift when a will is read.That is rarely about the money by that point. It is about having been kept in the dark.The paperwork checklist None of this needs a team of lawyers, but a few basics are worth having in place before the money moves.A decision on gift vs. loan, made deliberately rather than by default.A deed of gift or written record, if it is a gift, particularly for larger sums. Ideally, this should be prepared or reviewed with legal advice, so the intention and source of funds are clear.A loan agreement, if it is a loan - amount, interest, if any, repayment terms, and what happens on an early property sale.A lawyer's involvement, even briefly, for anything beyond a modest sum. Family money is still money, and a short consultation can be useful protection against an expensive dispute.A clean transfer record - bank transfer with a reference note, rather than cash - so the source of funds is easy to explain if a bank or, much later, a court ever asks.A conversation with other children, where relevant, so the decision does not come as a surprise.A review of your own retirement and housing plan, especially if the money affects your CPF, cash reserves, right-sizing timeline, or future healthcare buffer.Back at the Lims' dinner table By the end of the evening, Wei Ming and Yvonne have not changed their minds about helping Charmaine.But they have agreed to structure it as a documented loan rather than an informal gift, mostly because it keeps things clearer if their younger son needs similar help in a few years. They have also agreed to sit down with their own retirement numbers before finalising the amount.That is really what this decision comes down to.Not whether to help - most families have already answered that - but whether the help is built to last as well as the relationship it is meant to protect.Before the money moves, it may help to map out the purchase properly and whether it still protects both generations' plans. A PropNex salesperson can walk your family through the key property numbers, from cash and CPF to loan limits and overall affordability, before you decide how much help to give. Views expressed in this article belong to the writer(s) and do not reflect PropNex's position. No part of this content may be reproduced, distributed, transmitted, displayed, published, or broadcast in any form or by any means without the prior written consent of PropNex. For permission to use, reproduce, or distribute any content, please contact the Corporate Communications department. PropNex reserves the right to modify or update this disclaimer at any time without prior notice.

Read More

Resale Condo Market Watch in June 2026

Subdued resale condo market activity in June Sales activity in the overall property market pulled back further in June, including the resale condo market - largely due to the seasonal lull amid the June school holidays. About 888 condo units worth $1.86 billion was resold during the month - compared with the 976 resale transactions valued at $2.07 billion transacted in May. In June, resales transactions accounted for 82.5% of non-landed transactions, while new sale transactions accounted for 13.9% of transactions, reflecting the highest resale proportions on record since December 2025 (79.3%) (see Chart 1). Chart 1: Proportion of private non-landed transactions (excl. EC) by sale type by monthSource: PropNex Research, URA Realis Despite the slower new launch activity during the month, the average unit price of new non-landed homes continued to pick up from the previous month. The average new sales price grew 4.1% month-on-month (MOM) to $2,558 psf in June, while the average resale unit price slipped by 10.3% MOM. As such, the new sale and resale price gap crept up from 39% in May (see Chart 2), to 45% in June. Chart 2: New sale and Resale Price gap of non-landed homes (overall) by monthSource: PropNex Research, URA Realis Improving gains amongst resale transactionsIn terms of profitability, resale condo units transacted in June saw smaller gains compared with the previous month. Analysing the profits reaped by resale non-landed private homes in May 2026 and June 2026, it was found that resale condo deals in June garnered more profits. The proportion of loss-making transactions was higher in June 2026 over the previous month. The resale profit analysis involves computing gains achieved for the units by matching the condo resale transactions in May against their respective previous purchase price, according to caveats lodged. The study showed that 17.7% of resale condo transactions (146 deals) in June made more than $1 million in profits, a higher proportion compared with May (15.1%). Of these million-dollar profit-making deals, the deals was well spread amongst the three market segments, 39% in the Rest of Central Region (RCR), 31.5% in the Outside Central Region (OCR) and 29.5% in the Core Central Region (CCR) homes. Loss-making deals in June accounted for 5.2% of transactions, lower compared with the proportion of loss-making deals (6.5%) in May (see Chart 3). Chart 3: Proportion of profit quantum of resale non-landed transactions (May 2026 vs June 2026)Source: PropNex Research, URA Realis The average profit was subsequently computed on a project basis. To minimise sampling errors, resale condominium projects that posted fewer than three transactions during the month are excluded from the study. Based on URA Realis caveat data analysed by PropNex Research, the most profitable condo for the month, was Bartley Ridge, within District 13, which pulled in an average profit of more than $727,000 across six transactions in June. It was also the most profitable condo project in the RCR for the month. In the CCR, the most profitable condo development in June was D'Leedon, a project located in District 10, which achieved an average profit of over $596,000, across nine transactions. In the heartlands or Outside Central Region (OCR), the most profitable project was Jewel @ Buangkok in District 6 which garnered an average profit of over $549,000 across five transactions. Top Resale Condo projects^ in terms of average gross profit* (June 2026)Project NameNo. of transactionsAverage Profit Gained ($)Average Annualized Profit (%)#Year completed RegionBARTLEY RIDGE6$727,3174.9%2016RCRJEWEL @ BUANGKOK5$604,2004.9%2016OCRD'LEEDON9$596,5923.0%2014CCRBOTANIQUE AT BARTLEY6$549,3155.0%2019OCRLAKE GRANDE7$461,4133.7%2019OCRRIVERSAILS5$460,4005.2%2016OCRHIGH PARK RESIDENCES5$454,2004.5%2019OCRQUEENS PEAK7$442,7173.3%2020RCRSTIRLING RESIDENCES8$430,5724.0%2022RCRCLAVON5$400,2004.9%2024OCRSource: PropNex Research, URA Realis^projects with fewer than 5 transactions in the month are excluded from this analysis*Gains are derived from the resale transaction for each unit against the unit's last caveated transaction; the average profit is determined on the profits of all resale transactions in the development which occurred during the month. The profit reflected is gross - it has not accounted for the applicable seller's stamp duties, interest payable, taxes and other relevant divestment costs.#Annualised Gains is the compounded annual rate of return which shows the rate of return over the time period between the point of resale and the property's last caveated transaction, expressed in annual percentage terms. The formula for determining this is simply: [(current resale price) / (purchase price)] time period in years-1Analysis was done based on available data from URA Realis Going by districts, resale homes in District 21 (Upper Bukit Timah, Ulu Pandan, Clementi) raked in the highest profits on quantum basis, with transactions reaping average gains of more than $924,000 per deal. In terms of annualised gains, resale homes in District 20 (Ang Mo Kio, Bishan, Thomson) enjoyed an average annualised profit of 5.4% per deal. Top 10 Resale Condo districts^ in terms of average gross profit* (June 2026)DistrictNo. of transactions**Average Gains ($)Average Annualised Gains (%)#D2128 $924,3674.0%D2023 $889,5625.4%D1569 $826,1234.2%D1128 $818,0492.6%D1057 $703,6222.5%D2227 $627,5764.3%D1639 $603,4603.9%D1327 $599,2004.5%D948 $550,8201.6%D556 $537,9793.5%Source: PropNex Research, URA Realis^Districts with fewer than 10 transactions during the month were excluded from this analysis*Gains are derived from the resale transaction for each unit against the unit's last caveated transaction; the average profit is determined on the profits of all resale transactions in the development which occurred during the month. The profit reflected is gross - it has not accounted for the applicable seller's stamp duties, interest payable, taxes and other relevant divestment costs.#Annualised Gains is the compounded annual rate of return which shows the rate of return over the time period between the point of resale and the property's last caveated transaction, expressed in annual percentage terms. The formula for determining this is simply: [(current resale price) / (purchase price)] time period in years-1Analysis was done based on available data from URA Realis**Resale units with no available last caveated transaction data are excluded from this analysis Analysing individual transactions by gross profit quantum, it was found that the top five gainers from each region ranged from $1.86 million to $4.15 million. The units which chalked up bigger gains were mostly sizeable large format condos that are more than 1,300 sq ft in size, and consisted mostly of older projects built in the 1980s to early 2000s. The respective holding periods for the most profitable resale properties were mostly beyond 16 years - the oldest being a unit held for more than 30 years. Top 5 Resale Condo transactions in June 2026 by gross profit by regionSource: PropNex Research, URA Realis*Gains are derived from the resale transaction for each unit against the unit's last caveated transaction; the average profit is determined on the profits of all resale transactions in the development which occurred during the month. The profit reflected is gross - it has not accounted for the applicable seller's stamp duties, interest payable, taxes and other relevant divestment costs.#Annualised Gains is the compounded annual rate of return which shows the rate of return over the time period between the point of resale and the property's last caveated transaction, expressed in annual percentage terms. The formula for determining this is simply: [(current resale price) / (purchase price)] time period in years-1Analysis was done based on available data from URA Realis**Resale units with no available last caveated transaction data are excluded from this analysis It was found that the overall most profitable transaction and top gainer in the CCR was for a 5th floor unit at Nassim Park Residences. It was resold for an estimated profit of $4.15 million, reflecting an annualised profit of 2.9%. Based on URA Realis caveat data, the 6,954-sq ft unit was first bought in May 2019 and subsequently resold for $22.95 million in June 2026, with a holding period of about 7 years. Completed in 2011, Nassim Park Residences is a freehold luxury condominium located along Nassim Road in Singapore's prime District 10. The development is within walking distance of Napier MRT station on the Thomson-East Coast Line and is situated close to several established schools, including Singapore Chinese Girls' Primary School, Singapore Chinese Girls' School, Anglo-Chinese School (Primary) and Anglo-Chinese School (Junior), while also enjoying convenient access to the Orchard Road shopping belt and the Singapore Botanic Gardens.The top gainer in the RCR in terms of gross profit was for unit transacted at Maple Woods, which fetched a gross profit of $3.77 million (annualised profit of 5.4%), based on caveats lodged. The 2,917-sq ft 10th floor unit was sold for $5.8 million, with a holding period of 20 years. Maple Woods is a freehold condominium located along Bukit Timah Road in District 21. The development was completed in 1997 and is within walking distance of King Albert Park MRT station on the Downtown Line. It is situated near several reputable schools, including Methodist Girls' School (Primary and Secondary), Pei Hwa Presbyterian Primary School, and Ngee Ann Polytechnic, while also enjoying convenient access to Bukit Timah Nature Reserve and a range of lifestyle amenities in the Bukit Timah area.Over in the OCR, the top gainer in June was a 9th floor unit located in The Hacienda in District 15. The 3,079-sq ft unit was sold for $5.25 million, achieving an estimated profit of $2.37 million - which reflects an annualised profit of 3.9% over a holding period of nearly 16 years. The Hacienda is a freehold condominium located along Hacienda Grove in District 15. The development is within walking distance of Siglap MRT station on the Thomson-East Coast Line and is situated near several well-regarded schools, including CHIJ (Katong) Primary, Victoria School, Victoria Junior College and St. Patrick's School, while also enjoying easy access to East Coast Park and the dining and retail amenities in the Siglap and Katong neighbourhoods. Amid a still-low interest rate environment and rising new launch prices, condo resellers June stand to benefit as some homebuyers June find themselves priced out of the new launch market and could consider options in the resale segment.

Read More

When 8 Is Worth More Than 4: How Number Superstitions Shape Property Decisions

TL;DR Lucky and unlucky numbers can influence property decisions, but they should never outweigh the fundamentals of a good home. While number superstitions affects buyer psychology and transaction prices, factors like location, price, and long-term demand remain far more important. Number preferences are deeply rooted in culture: In Singapore, many buyers favour numbers like 8 and avoid 4 due to their pronunciation and cultural associations, although interpretations differ across languages and communities. Research shows number superstitions have real market effects: Studies found that buyers are willing to pay premiums for "lucky" addresses and expect discounts for "unlucky" ones, particularly for larger homes and prestigious units. Developers cannot manipulate unit numbers: Singapore's fixed unit numbering system makes it possible to observe genuine buyer behaviour, rather than pricing influenced by selective numbering. An unlucky number can also create opportunity: Buyers who care less about numerology may be able to purchase an otherwise identical property at a discount, although resale outcomes still depend on future buyer preferences. Practical considerations still come first: Affordability, location, connectivity, and overall property quality have a much greater impact on long-term value than the number on the front door. Bottom line: Number superstitions can influence negotiations and buyer perception, but it should be treated as a secondary consideration. The best property decision is still one built on strong fundamentals, regardless of whether the unit ends in a 4 or an 8. You're looking to buy a new home, and you found two resale listings in the same development, same floor, same facing, similar renovation. One priced slightly cheaper than the other. Everything checks out on paper. Then you notice something that makes you hesitate.No, it's not the size or the condition of the house. It's that the unit number ends with a 4.Whether you see these numbers as tradition, superstition, or something in between, it's hard to deny that many people take it seriously. So even people who don't consider themselves superstitious would probably think twice about buying a house with a "bad" number, scared it might be harder to sell in future. Some would rather pay a bit more for the other unit and avoid the issue altogether.We joke about superstitious beliefs but we secretly feel a little pleased when we're assigned a "good" number. Most of the time, it's harmless fun. But when you're making one of the biggest purchases of your life, you might feel a little pressured. In this article, we will explore: Which numbers are lucky and which are not? So, what is the impact of number superstitions in real estate? Could an "unlucky" unit actually work in your favour? Has number superstitions become less important? So... would you buy the unit ending in 4? Which numbers are lucky and which are not?It depends. The same numbers can mean different things to different cultures. For example, the number 13 is often avoided in Western cultures, but Cantonese speakers see it as auspicious because it sounds like "guaranteed prosperity". Likewise, the number 666 has a reputation as the devils' number, and we see it a lot in horror movies. But in China, it has become a modern internet slang that means cool or impressive.In Singapore, where there is a large Chinese population, many traditions are influenced by Chinese culture, including some number superstitions. For one, we tend to label number four as inauspicious. The belief is somewhat rooted in linguistics. In Mandarin and Cantonese, four (?, s) and death (?, s?) have similar pronunciation. But rather than a coincidence, many people think of it as an omen.On the other hand, Eight (?, b?) is associated with prosperity (?, f?), because they're pronounced similarly. In many parts of Asia, these beliefs have become deeply woven into everyday life, whether you personally believe them or not. For example, some buildings don't have a Level 4. Instead, it's labelled as 3A, or the lift simply jumps from Level 3 to Level 5.On the flip side, number 8 is everywhere. Businesses and brands often incorporate "88" into their names because it's believed to symbolise double prosperity. They even pay extra for phone numbers ending in 8888.While 4 and 8 are by far the most well-known, they're not the only numbers that catch buyers' attention.Some people also consider 6 (?, li) to be auspicious because it is often associated with smoothness or things going well, especially through phrases such as ????, which conveys the idea of "everything will go smoothly". Another favourable number is 9 (?, ji?), which is associated with longevity and permanence.Certain number combinations are also considered attractive. For example, 168 (???) is commonly interpreted as "prosperity all the way", while 518 (???) is read as "I want to prosper". On the flip side, combinations involving 4 are often avoided by those who subscribe to these beliefs. For example, 14 sounds similar to "will certainly die" (??), 24 resembles "easy to die" (??), and 174 sounds like "die together" (???).Of course, these number superstitions aren't an exact science, and interpretations can vary depending on dialect, language and even personal beliefs. What one buyer sees as a lucky number, another may not think twice about. But when enough people share the same preferences, those perceptions can begin to influence real-world demand including in the property market. Enjoying our insights so far? Stay updated with the latest property trends, expert analysis, and market perspectives from PropNex. Join our mailing list So, what is the impact of number superstitions in real estate?As much as they'd like to, developers cannot simply skip "unlucky" unit numbers to make a project more attractive. Government regulations require unit numbering in high-rise developments to follow a fixed format.This makes Singapore an ideal place to study whether numerology genuinely influences buyer behaviour. Since developers can't manipulate unit numbers, researchers can isolate the effect of the numbers themselves on property prices.A team of researchers from the National University of Singapore, Singapore Management University, and Nankai University did exactly that. They analysed thousands of private housing transactions and found that buyers were willing to pay more for homes with "lucky" addresses while expecting discounts for "unlucky" ones.Interestingly, the premium was larger for prestigious purchases: 8% more for larger homes and 7% more for top-floor units. In that sense, a lucky unit number can also be seen as an extra status symbol.The study also observed fewer property transactions taking place on dates considered inauspicious in the Chinese lunar calendar. This suggests that these beliefs can shape not just what people buy, but also when they choose to buy.Of course, a unit number isn't going to outweigh factors like location, connectivity or price. But when buyers are deciding between two otherwise similar homes, numerology can become the deciding factor. And the evidence suggests that enough buyers value it for those preferences to show up in actual transaction prices.Could an "unlucky" unit actually work in your favour?Here's an interesting thought.Suppose you bought a home with an inauspicious unit number at a discount because some buyers were put off by it. Years later, when it's time to sell, your buyer happens to be someone who doesn't believe in numerology at all. Maybe they're not Chinese-speakers. Or perhaps they're more concerned about the layout, location and price.In that case, you wouldn't have to offer the same discount when it's your turn to sell. If everything else about the property stacks up, your property could potentially outperform the "lucky" one.That being said, there's no way of knowing who your future buyer will be. So it's more like a game of chance than a proper strategy. If your eventual buyer is informed about the role numerology plays in real estate, they may expect the same discount you received years earlier. You're basically passing on the lower purchase price to the next owner.Has number superstitions become less important?There isn't definitive evidence to say that it has. However, Singapore's property market has changed dramatically over the past two decades. Homes have become more expensive so buyers are putting more focus on practical considerations such as affordability, commuting time, or proximity to good schools.Regardless, buyers who are familiar with these beliefs often continue paying more for lucky addresses, even if they aren't particularly superstitious themselves, simply because they expect the next buyer to care.Just like designer handbags or limited-edition watches, you might not personally think they're worth the premium, but if you know someone else will, you're more willing to pay today's price because you expect to recover it later.As long as people believe future buyers will continue valuing lucky numbers, those premiums can persist.So... would you buy the unit ending in 4?Let's go back to where we started.Two units: same project, same floor, same facing, same renovation. The only difference is the number on your address.If the unit ending in 4 is noticeably cheaper, would you take the discount? Or would you happily pay a little more for the peace of mind that comes with an auspicious address?After everything you've read, have you changed your mind?There's no right or wrong answer. Some buyers will gladly pay more for the peace of mind. Others will see an opportunity to buy the same home for less.Ultimately, lucky numbers should be seen as one factor among many, not the reason to buy or walk away from a property.A unit number may affect buyer psychology. It may help you negotiate. It may even influence how future buyers perceive the home. But it should not outweigh the fundamentals that matter more over time: location, connectivity, liveability, development quality, entry price, and long-term demand.It would not make sense to buy a property just because it ends with an 8. At the same time, it may be short-sighted to reject a fundamentally sound home simply because it ends with a 4, especially if the pricing already reflects that concern.The smarter question is not whether the number is lucky. It is whether the property still makes sense when the number is taken out of the equation. Views expressed in this article belong to the writer(s) and do not reflect PropNex's position. No part of this content may be reproduced, distributed, transmitted, displayed, published, or broadcast in any form or by any means without the prior written consent of PropNex. For permission to use, reproduce, or distribute any content, please contact the Corporate Communications department. PropNex reserves the right to modify or update this disclaimer at any time without prior notice.

Read More

Cold Prospecting for Real Estate Agents: Making First Contact More Relevant

Cold prospecting is difficult. Not because the skills are complicated - they are not - but because the contact has no reason to care yet. You are interrupting their day to ask for attention you have not earned.That is the challenge. Relevance is the answer.A cold message that is specific, timely, and clearly useful gets read differently from one that is generic. 'Hi, I am a property agent. Let me know if you need help.' goes nowhere. 'I work specifically in [estate] and noticed a few transactions this month that may change what sellers in your block can realistically expect - happy to share a quick update if that is useful' earns a reply, even from people who were not thinking about property.Relevance is the entry feeWhy are you contacting this specific person? The more precise and honest the answer, the better your opening. Relevance can come from geography - you work their estate actively. From timing - their property type has seen recent movement. From trigger events - a new MRT line, a school zone change, a nearby TOP that affects comparable prices.Vague relevance ('I help people with property') is no relevance at all. Specificity signals that this message was not sent to a thousand people this morning - which it probably was, but it should not feel that way.Keep the opening shortCold messages should not be presentations. They should establish three things in under 80 words: who you are, why you are reaching out now, and one simple question. Long paragraphs are discarded before the second sentence.Example: 'Hi, I am [Name] from PropNex, focusing on [area]. Recent transactions around [development/block] have raised some new pricing questions for owners there. Would a quick updated range for your unit be useful, or are you not reviewing this at the moment?' Clear. Respectful. Easy to answer.Comply first, prospect secondSingapore's Do Not Call registry, PDPA obligations, and CEA practice guidelines shape how and where cold outreach is permissible. These are not bureaucratic inconveniences - they exist for good reasons, and agents who ignore them face real professional and legal consequences.Before any cold outreach campaign, verify compliance requirements with your agency. Use approved contact lists and communication channels. Ethical prospecting is not only about avoiding penalties; it produces better-quality leads, because prospects who feel respected are far more likely to engage than those who feel spammed.Follow up with restraintTwo to three touchpoints is the appropriate ceiling for a cold prospect who has not responded. One initial message. One relevant follow-up with a useful resource. One closing message: 'I will leave this with you - feel free to reach out if the topic becomes relevant.' After that, move them to long-term nurture or close the lead. Repeated contact with someone who has not responded is not persistence; it is pressure.Common mistakeMaking the message about your need for leads. The prospect does not care about your pipeline. They care whether your message is relevant to their situation. Write from their perspective, not yours.Practice exerciseWrite a cold outreach message for three scenarios: an owner in an active resale estate, a landlord approaching lease expiry, and a buyer who attended an open house two weeks ago. Keep each under 80 words. Read each back and ask: 'Would I reply to this if I received it?' Views expressed in this article belong to the writer(s) and do not reflect PropNex's position. No part of this content may be reproduced, distributed, transmitted, displayed, published, or broadcast in any form or by any means without the prior written consent of PropNex. For permission to use, reproduce, or distribute any content, please contact the Corporate Communications department. PropNex reserves the right to modify or update this disclaimer at any time without prior notice.

Read More

Prospecting Discipline: Building Daily Habits That Create Future Appointments

Prospecting is the first activity to disappear when agents get busy. It is also the last thing that should.The irony is reliable: an agent lands a few deals, fills their days with viewings and paperwork, stops prospecting, and then - three months later - finds themselves with an empty pipeline wondering where the business went. The viewings and paperwork felt more urgent than prospecting. They always do. That is the trap.In Singapore's property market, where decision cycles are long, MOP timelines create natural lead windows, and clients often need multiple touchpoints before they are ready to act, prospecting is not a short-term activity. It is infrastructure. The conversations you start today become the appointments that appear six months from now.Prospecting belongs on the calendarIf it is not blocked, it will not happen. Full stop. Sixty to ninety minutes of focused prospecting, protected from viewings, portal browsing, and admin, is a non-negotiable daily appointment with your own future income.During that block, only one activity qualifies: starting or advancing conversations. Not designing social media posts. Not cleaning the database. Not reading market news. Prospecting time is for human contact - outreach, follow-up, and responses to warm leads. Everything else gets scheduled separately.Separate prospecting from nurturingThey feel similar. They are not. Prospecting creates new pipeline entries. Nurturing maintains existing ones. If your entire prospecting block is spent sending market updates to contacts who already know you, you are nurturing - which has its place, but is not the same as growing.A functional week might look like this: new cold or warm outreach on Monday and Wednesday, dormant lead reactivation on Tuesday, referral requests from satisfied clients on Thursday, and database review on Friday. The exact structure matters less than the intentionality. Each type of activity serves a different function.Scripts are starting points, not ceilingsSome agents avoid scripts because they worry about sounding robotic. That concern is valid - but the solution is to internalise the structure, not abandon it. A script provides the skeleton: reason for contact, relevant insight, one question, clear next step. The tone and language become yours with repetition.'I am reaching out because recent activity in your estate has shifted the pricing conversation - some sellers are still expecting last year's momentum, but buyer behaviour has become more selective. Are you monitoring your home value with any particular intention, or just staying informed?' That structure can be delivered naturally once the agent has said it fifty times.Measure leading indicatorsClosed deals are lagging indicators. By the time they appear, they reflect prospecting decisions made months earlier. What you can actually manage, in real time, are leading indicators: conversations started, replies received, appointments requested, referrals asked for, follow-ups completed.Tracking these reveals where the breakdown is. Low reply rates point to message quality. High replies but few appointments point to offer clarity. Many appointments but poor conversion points to consultation skills or trust. Each diagnosis suggests a different fix.Common mistakeWaiting to feel ready before prospecting. The confidence comes after repetition. Not before.Practice exerciseDesign a five-day prospecting plan. For each day, write the target audience, number of contacts, the message angle, and the follow-up action. Keep it realistic - something you would actually execute next week, not an ideal version of yourself. Views expressed in this article belong to the writer(s) and do not reflect PropNex's position. No part of this content may be reproduced, distributed, transmitted, displayed, published, or broadcast in any form or by any means without the prior written consent of PropNex. For permission to use, reproduce, or distribute any content, please contact the Corporate Communications department. PropNex reserves the right to modify or update this disclaimer at any time without prior notice.

Read More

Warm Market Prospecting: Starting Conversations Without Damaging Relationships

The people who already know you are your warmest leads and your most delicate asset. Handle them well and they become a self-renewing source of business. Handle them poorly and they quietly shift from supporters to avoiders.Warm prospecting in Singapore carries specific social pressure. The country's tight professional and community networks mean that a bad interaction travels. A friend who felt pushed now mentions it to a mutual contact. An ex-colleague who received three unsolicited sales pitches stops responding to anything property-related. These are small losses that compound.The agents who build strong warm networks do so by making their professional value genuinely useful - not by treating every personal relationship as a sales opportunity in waiting.Warm does not mean entitledKnowing someone does not give you the right to their attention or their referrals. Familiarity is the starting point, not the advantage. The relationship must be active and reciprocal before the professional element can enter.If you have not spoken to a contact in two years, do not open the conversation with a property pitch. Reconnect first - genuinely, not performatively. Ask about them. Find out what has changed. Establish that the relationship exists again before you put anything professional in front of it.Give your network a clear memory hookMost people in your warm network understand vaguely that you do property. That is not enough to generate referrals. They need a specific mental hook - a clear scenario they can recognise and attach your name to.'I mostly work with sellers who are trying to maximise their resale flat's exit value before upgrading.' 'I focus on helping young couples understand their first private property options.' 'I work with landlords who want to restructure their portfolio without triggering unnecessary ABSD.' Specific language gives people something to remember - and more importantly, something to repeat.Use education as a bridgeSharing a useful article, a market insight, or a relevant checklist opens a conversation without the weight of a sales ask. The message feels like help, not prospecting - and if it is genuinely useful, that is exactly what it is.'This might be relevant - I know you mentioned you have been watching what neighbouring flats are selling for.' That personalised line transforms a generic content share into something the recipient notices. It signals you were paying attention, which is the foundation of a relationship worth having.Ask specifically when the time is right'Do you know anyone buying or selling?' is almost impossible to answer. 'I am currently helping a couple of owners whose listings have stalled - usually a positioning issue rather than a price one. If anyone you know is in that situation, I would be happy to give them a no-obligation perspective.' That is answerable. The person can picture someone or they cannot.Common mistakeAssuming familiarity means permission. Warm prospecting earns the right to a professional conversation by protecting the personal relationship first.Practice exerciseWrite a message to a contact you have not spoken to in over a year. It should reconnect genuinely, mention your current advisory focus in one sentence, and offer one useful resource without asking for business. Keep it under 80 words and read it back as if you were receiving it. Views expressed in this article belong to the writer(s) and do not reflect PropNex's position. No part of this content may be reproduced, distributed, transmitted, displayed, published, or broadcast in any form or by any means without the prior written consent of PropNex. For permission to use, reproduce, or distribute any content, please contact the Corporate Communications department. PropNex reserves the right to modify or update this disclaimer at any time without prior notice.

Read More

Buyer Presentation: Comparing Options Without Creating Decision Paralysis

Give a buyer ten options and watch them stall. Give them three, framed around a clear trade-off, and watch them decide.Decision paralysis is not a personality trait. It is a design failure. When buyers are presented with too many choices, too many data points, or options without a clear framework for comparing them, the safest response is to wait. Most agents interpret this as the buyer needing more time. What the buyer actually needs is less - less information, fewer options, and more clarity about what matters most to them.In Singapore's property market, where buyers compare across HDB resale, Executive Condominiums, new launch private condominiums, and resale private units - each with different ABSD implications, CPF eligibility conditions, TOP timelines, and price trajectories - the risk of overwhelming a buyer is especially high. The agent's job is to cut through complexity, not add to it.Rank criteria before comparing propertiesBefore showing a single listing, understand what this buyer values most. Not in general terms - specifically. Is proximity to a school the non-negotiable, or is it a preference? Is timeline flexibility available, or are they on a hard deadline from lease expiry? Is capital appreciation the primary objective, or is this primarily a home for the next ten years?Once you have ranked their criteria, the shortlist almost builds itself. The properties that survive the filter are the ones worth discussing in detail. Everything else is noise.Limit options to three to fiveThree to five options. Each representing a meaningfully different strategic path - not just three listings from the same development at different floor levels.One option might offer the strongest location with a higher entry cost. Another offers better value per square foot but requires more patience on appreciation. A third is the compromise - not the best on any single dimension, but the least exposed on all of them. When each option represents a different set of trade-offs, the buyer's choice reveals something useful about their actual priorities.Explain trade-offs honestlyEvery property choice involves sacrifice. Say so directly. 'This option is strong on lifestyle and connectivity. The compromise is space.' 'This project has better growth fundamentals in the medium term, but the completion date means you will need to manage your current lease carefully.' Honest trade-off language builds trust. It also protects you - if the client later feels a downside was not mentioned, they remember that.End with a clear next stepA buyer presentation should not end with the buyer knowing more but still stuck. Conclude with a specific pathway: which two options to view this weekend, which financing assumption to verify with the bank first, which project showflat is worth attending before deciding. Give them one concrete next action. Not three. One.Common mistakePresenting options without first establishing what the buyer values most. More listings do not automatically help. Better-filtered listings, explained with clear trade-offs, do.Practice exerciseBuild a comparison table for three property options using five criteria: affordability, timeline, space, location, and exit audience. Add one sentence below each option explaining who it suits best. Present it to a colleague and ask whether the trade-offs are genuinely clear or still require more explanation. Views expressed in this article belong to the writer(s) and do not reflect PropNex's position. No part of this content may be reproduced, distributed, transmitted, displayed, published, or broadcast in any form or by any means without the prior written consent of PropNex. For permission to use, reproduce, or distribute any content, please contact the Corporate Communications department. PropNex reserves the right to modify or update this disclaimer at any time without prior notice.

Read More

Property Presentation Skills: Explaining Complex Decisions Without Overwhelming Clients

More information does not produce better decisions. It produces exhausted clients who postpone.This is the core failure of most property presentations. The agent arrives prepared, lays out every relevant data point, explains the financing options, walks through the comparables, and presents three scenarios. The client nods along, asks a few polite questions, and says they need to think about it. The agent leaves wondering what went wrong.What went wrong is that the presentation answered questions the client did not have, instead of the one question they did. Every client carries a specific decision - one that is keeping them stuck. Your job is to identify that decision and build everything around answering it.Start with the decision, not the dataBefore opening a slide or pulling up a transaction report, write the client's decision question at the top of your preparation. 'Should we sell first or buy first?' 'Is this unit priced fairly given what has sold nearby?' 'Can we upgrade comfortably, or are we stretching too far?' 'Should we wait for a better rate environment or enter now?'Every piece of information you present should connect to that question. If it does not help the client answer it, leave it out. Ruthless editing is a professional skill, not laziness.Use the three-layer structureContext, implication, recommendation. These three layers keep a presentation advisory rather than encyclopaedic.Context states what is happening: 'Recent transactions in this estate have clustered in this range.' Implication says why it matters to this client: 'Pricing much above that range typically reduces viewing quality within the first two weeks.' Recommendation is what to do next: 'We would position at the upper end of the defensible range and set a two-week review point.' Three layers. No filler. Clear conclusion.Simplify numbers without hiding riskSingapore property transactions involve CPF, cash, loans, ABSD, BSD, SSD, renovation costs, and legal fees - often simultaneously. Clients who see all of this at once shut down. Simplify the presentation, but do not oversimplify in ways that hide real risk.'This is the comfortable range. This is the stretch range. This is the range where I would be cautious.' Plain language. Clear categories. Then: 'The assumption behind the stretch scenario is that interest rates stay broadly where they are. If they move by 0.5%, the monthly difference looks like this.' Clients can handle honest complexity presented clearly. What they cannot process is complexity presented all at once without a frame.Make it a conversation, not a monologuePause at every decision point. 'Does this timeline match what you are planning?' 'Would this monthly commitment still feel comfortable if your household income changed?' 'Is your priority here capital growth, school proximity, or minimising downside risk?'These questions do more than gather information - they make the client part of the reasoning. When people participate in reaching a conclusion, they own it. They are not sold to; they are guided. That is a fundamentally different experience, and clients feel the difference.Common mistakeEquating the quantity of information presented with the quality of service delivered. Clients value clarity. A twenty-slide deck that ends without a clear recommended next step is not a service - it is a performance.Practice exerciseTake one client scenario and build a five-part structure: decision question, current market context, key numbers, options with trade-offs, and one clear recommended next step. Keep each section to three bullet points. Present it out loud to yourself, then cut anything that does not directly answer the decision question. Views expressed in this article belong to the writer(s) and do not reflect PropNex's position. No part of this content may be reproduced, distributed, transmitted, displayed, published, or broadcast in any form or by any means without the prior written consent of PropNex. For permission to use, reproduce, or distribute any content, please contact the Corporate Communications department. PropNex reserves the right to modify or update this disclaimer at any time without prior notice.

Read More

Listing Presentation: Winning Seller Confidence Before the First Viewing

A seller is not choosing a service provider. They are choosing a person to protect the most valuable asset they own, manage a negotiation that will shape their next decade, and represent them when things get difficult.That is the weight you walk into every listing appointment carrying. The agents who win consistently are the ones who feel that weight - and prepare accordingly.In Singapore's competitive agency landscape, sellers often interview two or three agents before deciding. They compare pricing opinions, they assess communication quality, and - whether they articulate it or not - they decide who they trust. A polished pitch that lacks substance loses to a plainspoken agent who clearly understands the property. Every time.Start with their objective, not yoursThe agents who lose listing appointments fastest are the ones who begin by talking about themselves. Track record, agency size, transaction volume - all of it matters, but none of it is why the seller called you.Open with questions. Why are they considering a move? What outcome do they need from the sale - a specific proceeds amount, a particular timeline, minimal disruption? What happens if the property takes three months longer than expected? What is their biggest worry about the process? The answers to these questions shape everything that follows, and they also communicate something more important than any credential: that you are listening.Diagnose before prescribingEvery property has a specific selling challenge. A ground-floor unit competing against better-facing stacks on the same development. A 30-year-old resale flat where the buyer pool is partly constrained by CPF usage limitations. A private condominium in an estate where new launch supply is about to increase competition.Name the challenge plainly. Sellers respect honesty far more than flattery. When you demonstrate that you have thought carefully about what this specific unit is up against, your proposed strategy becomes credible. You are not just promising to sell it - you are showing that you understand why it requires a strategy.Present marketing as a system, not a promise'I will post it online' is a promise anyone can make. A system is different. Walk through the sequence: professional photography and copywriting before listing, portal positioning with targeted exposure, social content to build additional reach beyond active portal users, buyer filtering to focus viewings on serious candidates, feedback reporting after each viewing, and negotiation follow-through when offers arrive.Each stage has a purpose. Each feeds the next. When sellers understand the logic of the sequence, they trust the plan rather than simply hoping you are good at your job.Set reporting expectationsSellers become anxious when they go quiet. Anxiety becomes interference. Set the reporting cadence before the listing launches: weekly updates covering enquiry volume, viewing quality, buyer feedback, competing listings, and any strategy adjustments. Make the service tangible from the start.Common mistakeMaking the entire presentation about your credentials rather than their property. Sellers care about your background, but they care more about whether you understand what you are walking into.Practice exercisePrepare a listing pitch for a property in a segment with slow market demand - perhaps an older resale unit in an estate with several competing newer listings. Write out the likely buyer profile, pricing logic, marketing sequence, and reporting plan. Present it to a colleague and ask them where they would question your reasoning. Views expressed in this article belong to the writer(s) and do not reflect PropNex's position. No part of this content may be reproduced, distributed, transmitted, displayed, published, or broadcast in any form or by any means without the prior written consent of PropNex. For permission to use, reproduce, or distribute any content, please contact the Corporate Communications department. PropNex reserves the right to modify or update this disclaimer at any time without prior notice.

Read MoreQuick insights you can apply immediately-from market indicators to financing perspectives.

Featured In-Person Learning Opportunities

Join our signature CES sessions to understand market trends, upgrading paths, and common property pitfalls — a helpful starting point before exploring deeper topics.

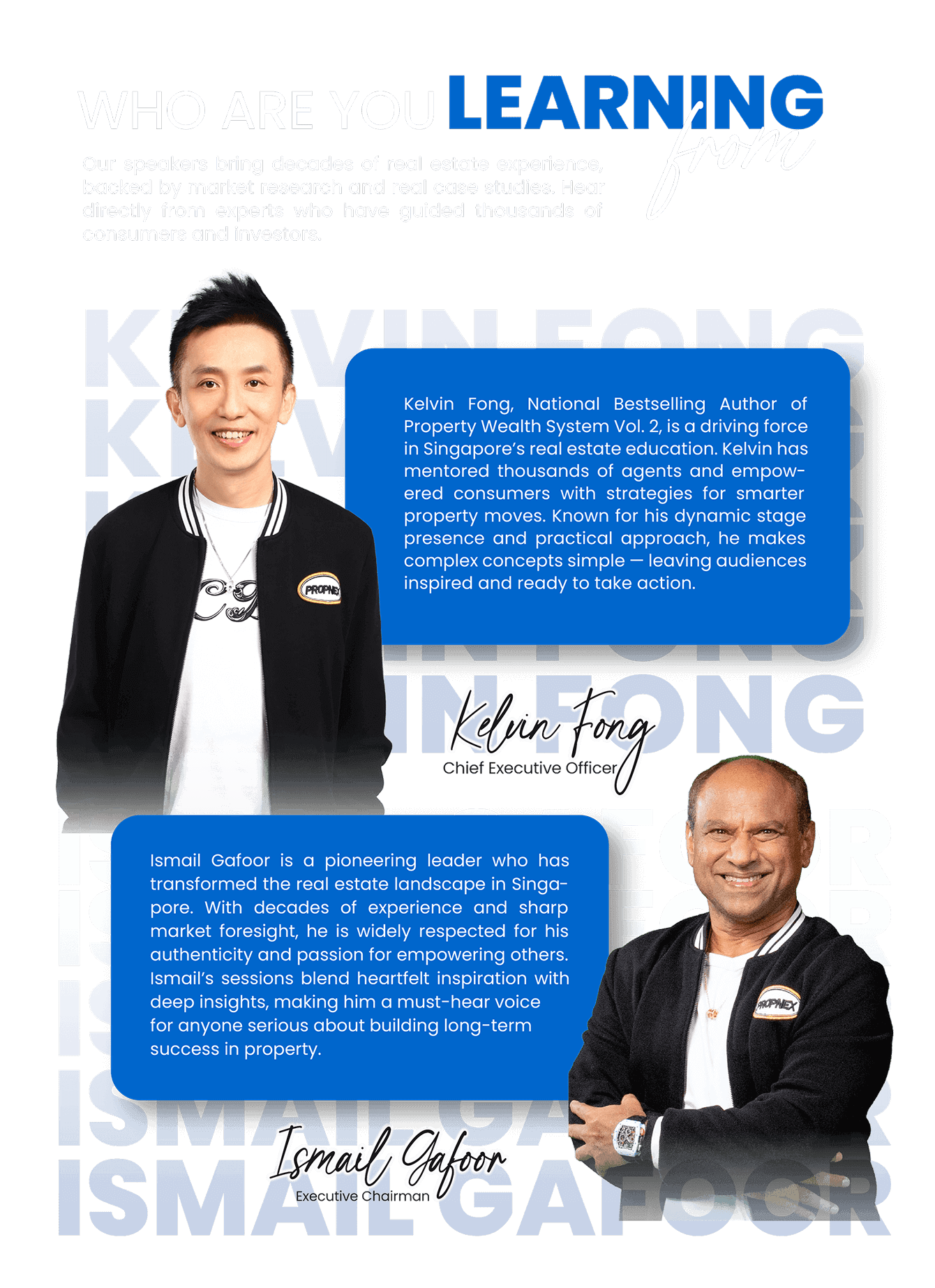

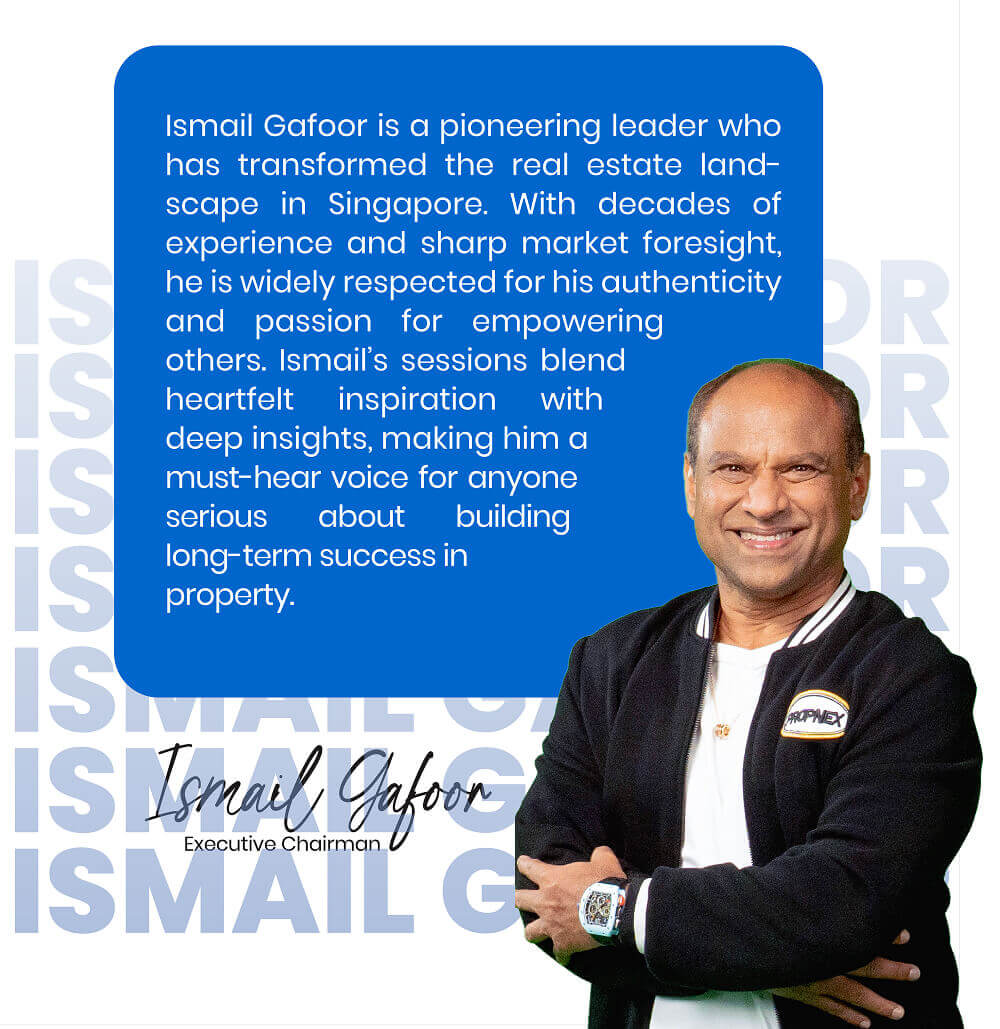

What People Say

Our speakers bring decades of real estate experience, backed by market research and real case studies. Hear directly from experts who have guided thousands of consumers and investors.

01 Are these seminars free to attend?

02 Who should attend?

03Do I need prior property knowledge?

04 Can I ask questions during the seminar?

05 Is this Learning Hub only about seminars?

Frequently

Asked Questions

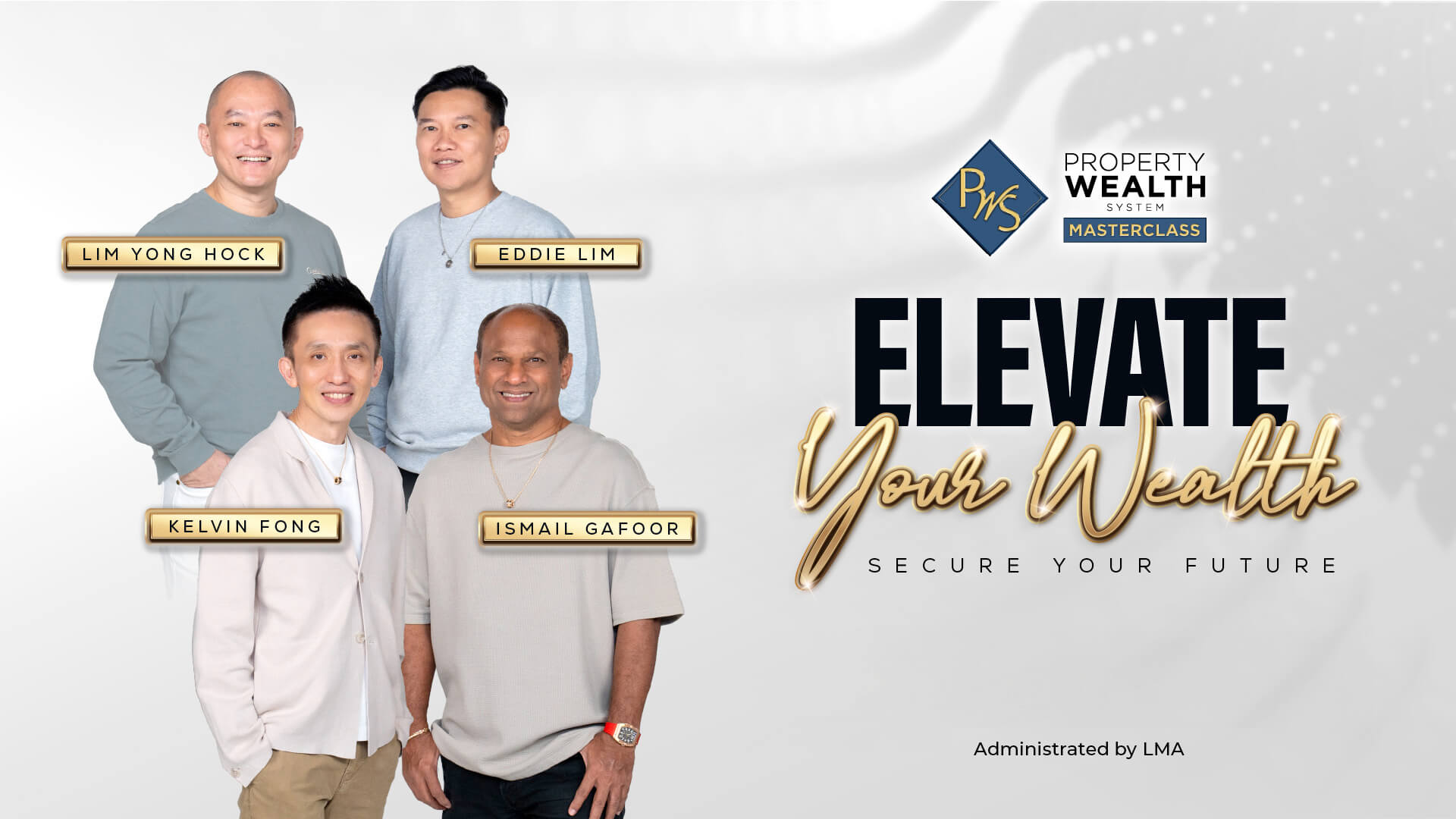

Deep-Dive Learning Pathways

Beyond introductory concepts, our PWS Masterclass offers a structured, hands-on approach for homeowners and investors ready to plan long-term wealth strategies.

For those who want to go deeper, the Property Wealth System (PWS) Masterclass is a 2-day immersive workshop where you’ll:

Apply the same frameworks you learned at CES in a hands-on way

Learn to calculate and assess your own property portfolio and “property health”

Build a clear, step-by-step action plan for long-term wealth creation through property

Think of CES as your starting point to understand the market — and PWS as your roadmap to take decisive action with confidence.